Reiterating 'Buy' On These Picks

Reiterating 'Buy' On These Picks

Delek US Holdings, Mitek Systems and Nomad Foods

Highlights

The sum of the parts case for DK still looks attractive even with weakness in the company’s key asset.

External risks have been mitigated for MITK, but slowing first-half growth has sparked investor concern.

NOMD is cheaper than it was when we recommended it last year — yet earnings are higher. At less than 10x free cash flow, the company simply needs to hit guidance to drive solid upside in the stock.

This week, we return to three ideas from 2023 that still look attractive here in 2024 — even if the characteristics of the respective bull cases have changed.

The SOTP Risk For Delek

Back in January 2023, we took a long look at the dangers of “sum of the parts” bull cases. In many cases, the discount that exists on paper continues to exist in practice1 and the perceived upside doesn’t materialize;

So when we recommended refiner Delek US Holdings DK 0.00%↑ in April of that year, we were careful to highlight the risks. At the time, Delek had a market cap of $1.57 billion; its stake in midstream MLP Delek Logistics DKL 0.00%↑ was, on paper, worth $1.67 billion.

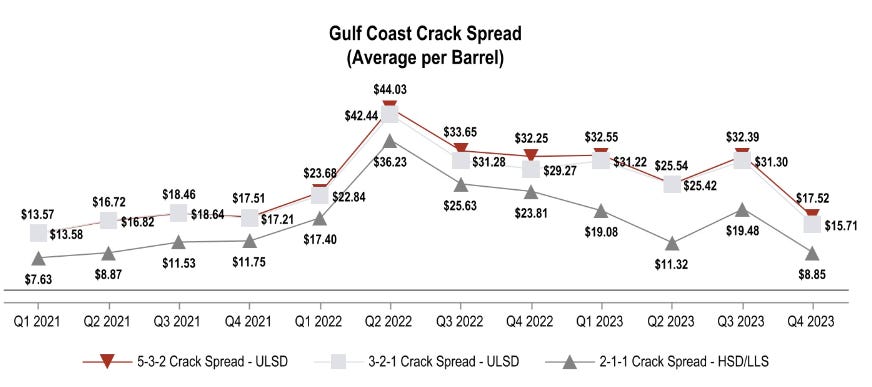

The big concern was that crack spreads would lead to sharply lower refining profits. Those spreads indeed narrowed amid post-pandemic normalization:

source: Delek 10-K, 2023

As a result, profits have been pressured. Q4 Adjusted EBITDA was down 71% year-over-year; the figure declined by nearly half in the first quarter.

The other issue is that Delek Logistics stock has faded: it’s declined 18% since we recommended Delek2. About two-thirds of the decline came in March, when the company priced a secondary offering of units well below market (and indeed modestly below Thursday’s close). That fade has cost Delek about $300 million in paper value, nearly 20% of its market cap 15 months ago.

And yet, to some degree, the performance of Delek over the past 15 months does support the original bull case. The stock still has returned nearly 10% including dividends, or about 7.8% annualized. That’s terrible in the context of the roaring S&P 500. But its not awful considering that something closer to the bear case than the bull case has played out3.

The Continuing SOTP Case For Delek

Delek’s market cap is almost exactly where it was last April, at $1.6 billion4. The value of its stake in Delek Logistics is no longer greater than its market cap, but it’s substantial: $1.37 billion at Thursday’s close.

What has changed, however, is the Delek balance sheet. At the end of 2022, net debt excluding Delek Logistics (which is consolidated into Delek’s financials) was $559 million. The figure after Q1 2024 was just $152 million.

And so the non-logistics part of Delek still seems to be valued at a ridiculously low level. Enterprise value is about $350 million (the $200 million in market cap above the value of the DKL stake, plus net debt excluding Logistics). Trailing twelve-month EBITDA is $437 million. Delek’s refining and retail business thus are trading at less than 1x EBITDA.

There’s in fact a case that the retail business, with $47 million in trailing twelve-month EBITDA, pretty much covers the $350 million EV: majors Murphy USA MUSA 0.00%↑ and Casey’s General Stores CASY 0.00%↑ trade at about 12x, while Delek’s retail business alone is valued at 7.4x. That leaves the refining business — with $390 million in TTM Adjusted EBITDA, less corporate costs — available for free.

The Risks And The Reward

Of course, “for free” is a common part of SOTP cases. And there are some pretty clear risks here.

Among them is management. Chief executive officer Avigal Soreq took over in June 2022, and has added new executives (including the Chief Commercial Officer and Chief Technology Officer) since then. As we noted last year, Soreq and other executives promised to work on narrowing the SOTP discount; on the Q1 2023 call, the CEO told an analyst, “We have a line of sight that is going to be very accretive to both DK and DKL. And I'm sure that you're going to be very happy.”

A year-plus later, there really hasn’t been any progress. There’s been a lot of vague talk about doing something with DKL, and in fact the company highlighted the unit offering at the subsidiary as an accomplishment, despite the decline in DKL shares:

source: Delek US Holdings Q1 2024 earnings release (author highlighting)

It does seem like Delek’s mid-term plan is to find an owner for a larger part of DKL, which would allow the company to deconsolidate the subsidiary. Whether that necessarily moves the needle is unclear: it’s not that difficult to do the math above, and a brief search on X shows a number of funds making the same SOTP case.

Meanwhile, operational improvements clearly have occurred at the company’s three major refineries, but there’s also been a number of hiccups that have kept the company from hitting a mid-$5 per barrel cost target, planned now for the end of the year. There’s definitely a sense that, overall, Delek isn’t moving fast enough or efficiently enough to capture the paper value of the various businesses, or to drive cost improvements at the refinery level5.

But there are signs of progress. After Q1, Delek floated the idea of selling the retail business; the company has engaged an investment business to evaluate alternatives there. Meanwhile, the marketing business posted an awful first quarter, with a $65 million EBITDA loss. There should be room for improvement there, as management’s unofficial guidance in the past has been profits in the unit.

It’s not necessarily stunning that management isn’t moving quickly. As is often the case with SOTP valuations, there isn’t necessarily an easy path to unlocking value. Delek can’t just sell its now-72% stake in Delek Logistics for the market value and send the cash back to shareholders. Delek Logistics’ MLP status adds tax complications as well.

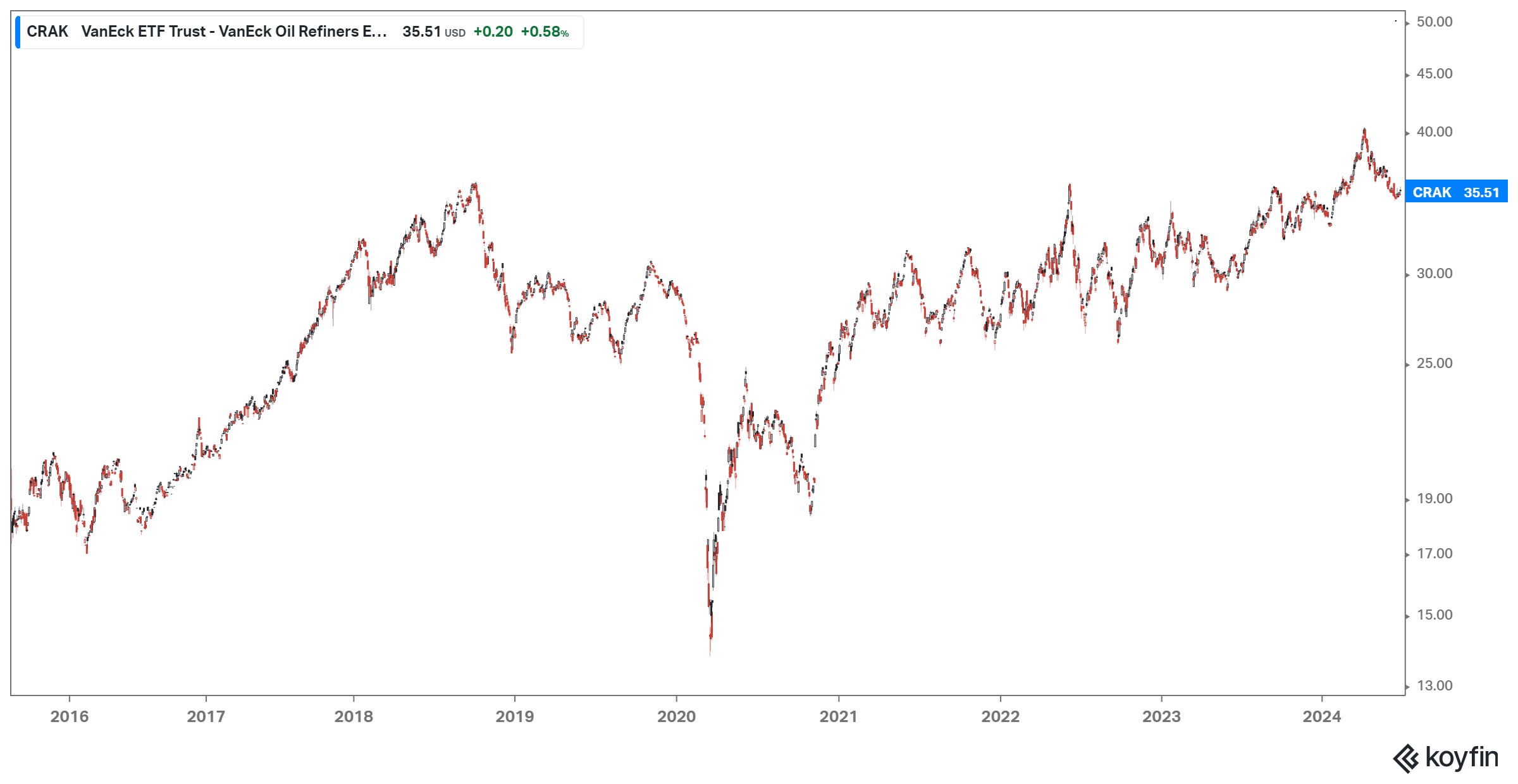

Overall, though, there’s enough potential reward. Refinery stocks are doing well, as the lower rate of electric vehicle adoption (and strong demand for air travel) has mitigated concerns of a peak in demand:

source: Koyfin; chart of VanEck Oil Refiners ETF CRAK 0.00%↑

There are an absolute ton of variables here, ranging from natural gas prices (a key input cost, and thus beneficial at the moment) to spreads (normalizing) to broader oil prices.

Still, the value on paper is such that it doesn’t take that much for management to unlock it. That might be through a major move with DKL, or with retail, or simply by driving continuing free cash flow. Executive Vice President of Operations said after Q1 that he believed mid-cycle EBITDA was $750-$800 million for the entire company; including DKL and its debt, that values Delek at likely under 5x EBITDA6. Refiners are cheap on an EV/EBITDA, but midstream and retail multiples suggest that blended figure is simply too low.

Given that Delek has still provided some returns with little movement, there still seems to be a solid risk/reward here. It’s not clear exactly what management will do, or when it will move, but there clearly is something coming. It already has taken some patience, and may require some more, but we still believe DK has a catalyst on the way and, eventually, a big move up.

Mitek Systems: Risks Go Down, And Up

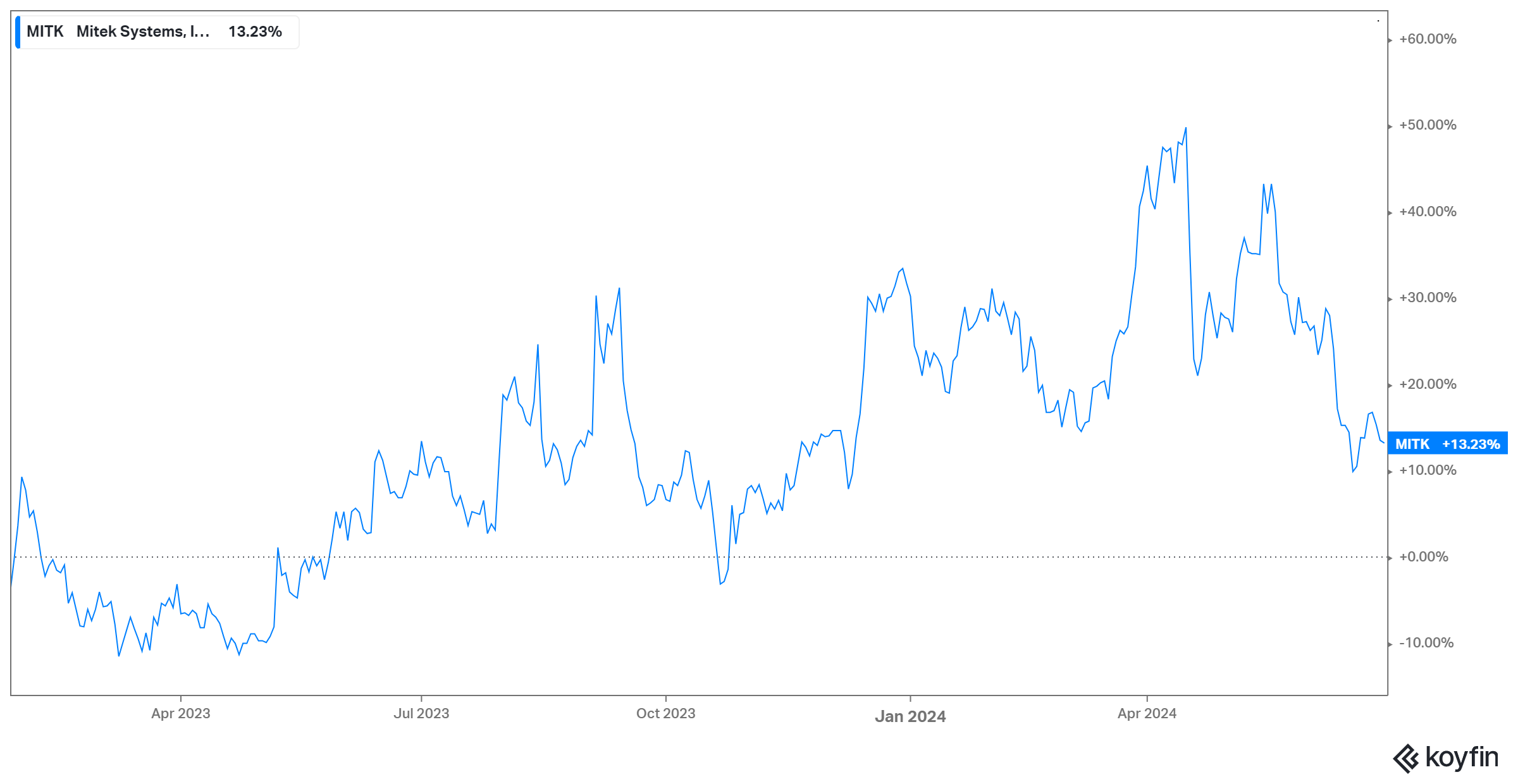

Mitek Systems MITK 0.00%↑ is up 13% since our bull call in January 2023, but of late has been dead money: shares are actually down 14% over the past year. A poor response to fiscal Q1 earnings in April is the primary catalyst; Mitek again reiterated its full-year guidance after the Q2 release in May, but investors seem unconvinced.

source: Koyfin

Readers may have noticed the odd cadence of the quarterly releases, but that is a big part of the story here. Mitek spent two years dealing with delayed financials, but has finally caught up with no apparent sign of significant misstatements.

That was one of the major concerns facing MITK at the time of our call. Another was patent litigation by USAA, which had sued several financial institutions over the use of patents covering check capture technology. Mitek and USAA both claimed to have invented the technology; though the two companies settled their own litigation in 2014. One clear risk has been that USAA will turn its sights back on Mitek eventually.

There, too, there is good news. As Mitek leadership noted last year, five USAA patents already have been invalidated, which brings some of the major judgments into question. The risk of a patent war remains, but seems mitigated. Were Mitek an eventual target, one imagines the suit would have been filed by now.

The idiosyncratic risks thus seem relatively muted. What seems to be spooking the market of late is a notable slowdown in growth. Mitek’s deposits business, based on that check capture technology, had been a steady double-digit grower, but first-half fiscal 2024 revenue is down 14%. Mitek did have a one-time $7 million boost in Q1 2023, and a record Q2, so comparisons matter, but even in that context growth has clearly slowed. And so the worry is that the secular decline of the check is catching up with Mitek, which to date has offset that decline with pricing power and growing market share for mobile check capture versus physical deposit.

Meanwhile, the company’s Identity verification business, built largely through acquisitions, has also stagnated. First-half revenue is up less than 2% year-over-year, after 17% growth last year.

And so the case relative to where it was almost 18 months ago seems like a mixed bag. The worries outside the business seem less pressing; but now the concern shifts to the business itself.

The Case For MITK

All that said, at its core the bull case for MITK is not terribly different from what it was early last year. The promise still comes from a deposits business that seems undervalued, along with optionality from the efforts in ID verification.

As we noted last year, Mitek basically has a monopoly in check capture. And that leads to enormous profit margins. The company is guiding to non-GAAP operating margins of 30% to 31% this year — even with the ID verification business forecast to be unprofitable. That guidance gets adjusted EPS to about 75 cents per share, implying a P/E multiple of about 15x7. Given losses in verification, the multiple assigned to the check business is even lower; even adding back stock-based compensation (~$15 million this year, though that figure may be somewhat elevated), P/E is a little over 20x.

For a monopoly business that is still guided to drive growth (excluding last year’s one-time boost, management expects revenue to rise 12% for the full year), that multiple is too low. Meanwhile, the ID verification business, despite its stumbles, offers some interesting promise. The rise of generative artificial intelligence is making scams more common and more complex; Mitek’s biometric solutions offer a potential defense. Mitek is seeing particular interest in its Check Fraud Defender product, and growth there should offset some declines in legacy products. The move to segment profitability also augurs a step up in margins and profits in fiscal 2025.

Along with Q2 earnings, Mitek did, somewhat surprisingly, fire its CEO. The explanation from the board is that the company needed new leadership after several years of basically crisis management; it’s an explanation that seems at worst reasonable.

That CEO, Max Carnecchia, did resign from the board earlier this month despite promising to stay on through the appointment of his replacement. That might suggest some disagreements over strategy and capital allocation, particularly given that the board announced a $50 million buyback program alongside the Q2 release. That program is material in the context of a $525 million market cap, but more importantly it cements the idea that Mitek isn’t out looking for more acquisitions8.

On the whole, then, MITK looks exceptionally intriguing. There’s hope for support for the stock from the buyback, an undervalued monopoly business in deposits, and potentially secular tailwinds in ID verification if the company can improve execution there. As it was early last year, this remains a name that can easily provide triple-digit upside in a blue-sky scenario.

NOMD Looks Like An Even Better Buy

In March 2023, we called out European frozen food manufacturer Nomad Foods NOMD 0.00%↑ as a contrarian yet defensive play. To date, the call hasn’t worked; even with dividends (initiated this year), NOMD has posted total returns of -4.6%.

For the most part, the case is exactly the same. U.S. investors clearly are skeptical toward both growth and margins, and 2023 results seem to show why. Adjusted earnings per share declined 4.2% year-over-year to €1.61; perhaps most notably, volume/mix plunged 9.5%; Nomad meanwhile took a whopping 14.4% in pricing.

But that environment is normalizing. Inflation in the euro zone has come down sharply. Processed food, alcohol, and tobacco saw an incredible annualized inflation rate of 13.4% in May 2023; that figure now is under 3%. Nomad is forecasting a benefit from volume/mix in 2024, along with adjusted EPS growth of 9%-12%. There’s some benefit in there from share buybacks, but the outlook still implies modest EBITDA margin expansion as well. A solid Q1 report — NOMD rose 5% after the print — seems to support that guidance.

But with NOMD stock down since our call, the stock now looks even cheaper. At the midpoint of guidance, shares are trading at under 9x adjusted EPS and less than 10x free cash flow. That’s for a business still growing, and detailing aggressive plans to retake market share after focusing on margins during the heavily inflationary environment.

As we noted last year, this is a solid management team that’s been wise about capital allocation. After building heavily through M&A before the pandemic, it’s focused on optimizing operations during and after it. Although NOMD hasn’t been a strong stock, the results of the business have been solid:

source: Koyfin

There’s certainly the risk of another shock in Europe, and it’s possibly stocks in the region simply stay cheap. Investors spent literally decades waiting for Japanese stocks to rally after investors wrote that market off. But NOMD can be aggressive with buybacks (it bought back €7 million in shares in Q1, and we’d expect more as the year rolls on). Any growth at this valuation eventually leads to upside.

The sell-side remains optimistic, with an average price target above $24. That’s in the ballpark where we were last year — and it’s where we remain today. This is a stock that, properly valued, should have at least 20% upside: 12x $2 in 2025 adjusted EPS gets total returns near 50%. All NOMD needs to do is to keep executing, and change investor perception.

As of this writing, Vince Martin is long Delek US Holdings. He has no positions in any other securities mentioned, but may initiate a position in NOMD in the near future.

Disclaimer: The information in this newsletter is not and should not be construed as investment advice. Overlooked Alpha is for information, entertainment purposes only. Contributors are not registered financial advisors and do not purport to tell or recommend which securities customers should buy or sell for themselves. We strive to provide accurate analysis but mistakes and errors do occur. No warranty is made to the accuracy, completeness or correctness of the information provided. The information in the publication may become outdated and there is no obligation to update any such information. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Contributors may hold or acquire securities covered in this publication, and may purchase or sell such securities at any time, including security positions that are inconsistent or contrary to positions mentioned in this publication, all without prior notice to any of the subscribers to this publication. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.

In fact, the three names we covered closely in that piece — IAC Inc. IAC 0.00%↑, Cannae Holdings CNNE 0.00%↑, and VOXX International VOXX 0.00%↑ — have all declined since publication.

As in our previous piece, for clarity we’ll consistently refer to Delek US / DK as “Delek” and Delek Logistics Partners LP / DKL as “Delek Logistics”.

The decline in refining earnings is not a surprise, but the weakness in DKL is unexpected, given MLPs overall have performed reasonably well. And of course, an investor could have hedged out that weakness via a long DK/short DKL pairs trade, which would have improved returns to the low double-digits, when accounting for DKL dividends.

DK stock is up over that period because, thanks to stock buybacks, the share count has fallen.

Management has done a nice job at the corporate level thanks to a cost savings program, with spend there down $30 million in full-year 2023. Q1 was a disappointment with a $10 million increase year-over-year, though management attributed that to “the timing of employee costs”.

We’re assuming, roughly speaking, that Logistics EBITDA is $350-$400 million of that figure; excluding the ~28% “owned” by minority investors there, Delek US Holdings’ mid-cycle EBITDA is ~$675 million, implying a roughly 5x multiple on a $3.34 billion enterprise value ($1.6B market cap, $1.74B net debt including Delek Logistics).

At the midpoint of guidance, adjusted EBIT is $55.7 million. Interest expense is running at ~$9 million; for the sake of conservatism and understanding ‘true’ earnings power, we use an effective tax rate of 23%, though Mitek is guiding for 13% this year after the 23% figure the year before.

Executives have said as much for several quarters, but the authorization does add board-level support for those claims.