Research Notes: Catching Up On Some Picks

Research Notes: Catching Up On Some Picks

Following up on SCHW, HOOD, and SENEA

A quick update on some of our favorite ideas of late.

The Charles Schwab Pitch

We recommended Charles Schwab SCHW 0.00%↑ a little over a year ago. Silicon Valley Bank had just failed, and SCHW had declined 24%.

Our pitch contained 3,400 words, but in essence could be boiled down to just two: come on. Charles bleeping Schwab was not going bankrupt. Yes, as another writer calculated, the company’s tangible common equity was negative, when marking to market its long-term securities. But the mark-to-market losses were driven by interest rate moves, not credit quality. As long as there was no ‘run on the bank (or brokerage)’, the issue was one of earnings, not of solvency.

Over time, that case has been proven mostly correct: including dividends, SCHW has returned 43%. Investors who bought after the open the following Monday (myself included) have done better. But the S&P 500 has gained 32% on a total return basis, and Interactive Brokers IBKR 0.00%↑ has performed marginally better. Another name we floated at the time, regional bank-focused software provider Q2 Holdings QTWO 0.00%↑ has more than doubled1.

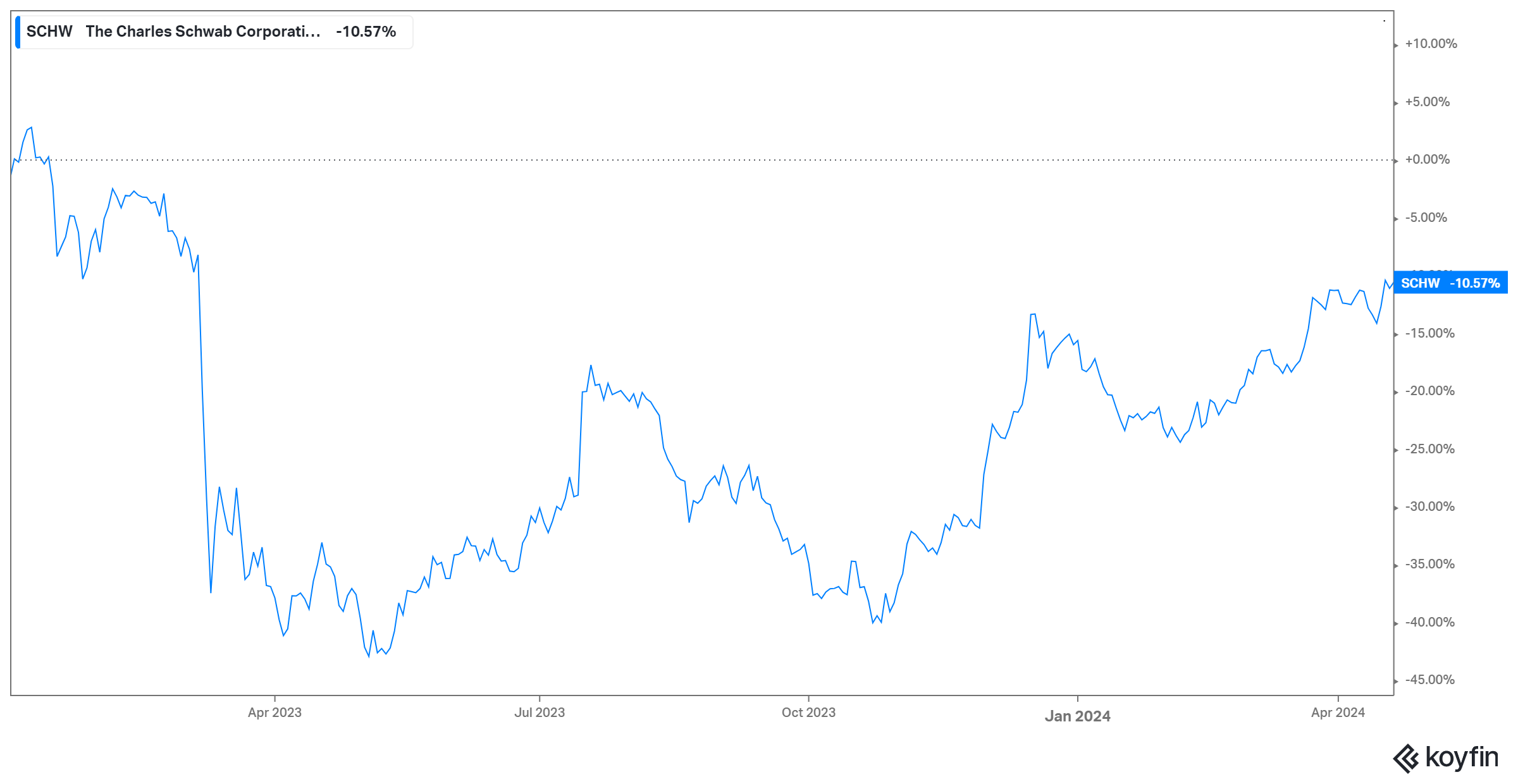

source: Koyfin; chart since 1/1/23 (we published March 12, immediately after the steep decline)

It’s been a good call, but with some volatility over the last year. The important question now is if SCHW is still a good call — which basically comes down to the question of whether the stock can recapture its pre-SVB levels.

Did SVB Change Schwab?

Obviously, to fully recover its losses, Schwab needs to do more than just not go bankrupt. The publicity surrounding the failure of SVB accelerated “cash sorting”, in which customers take their cash out of Schwab brokerage accounts (which, still, pay minimal interest) and transfer into higher-yielding instruments (including those offered by Schwab itself).

But as we pointed out at the time, that kind of activity wasn’t unusual in a rising interest rate environment. Importantly, nothing that happened in March 2023 was new. Schwab management knew it was going to face the effects of long-term bets on short-term results, but as lower-yielding paper matured, it would be able to roll those proceeds into higher-yielding alternatives, steadily boosting earnings.

For the most part, that’s played out. Schwab management does appear to have been a bit too optimistic in terms of cash sorting; its forecast for 2025 net interest margin was walked down a bit last year. Since then, however, management has remained optimistic, including through the Q4 2023 and Q1 earnings releases this year. Cash sorting has moderated significantly:

source: Charles Schwab Q1 business update presentation

The capital position is improving, net interest margin is on track, and Schwab sees “significant” further improvements in NIM long-term. A “higher for longer” scenario suggests more help from rates as well.

The bull case now still rests on a point we made last March: really, not that much has changed. SVB probably heightened awareness of cash sorting, but investors in February 2023 were long SCHW because higher rates would significantly boost earnings — eventually. In April 2024, there’s a strong case to own SCHW because…higher rates will significantly boost earnings, only a year or so sooner.

One counterpoint is that, on an MTM basis, the balance sheet still looks unwieldy. We continue to believe that is essentially immaterial. Barring regulatory intervention (highly unlikely) or significant solvency concerns that change customer behavior (even less likely), the issue remains one of earnings, not solvency. And that issue is one that will be fixed over time (unless rates collapse, but that’s not a risk unique to SCHW).

The more concrete concern is that the SVB crisis did change Schwab, if perhaps not in the ways that some bears argue. Customers are more aware of the better rates offered by other brokers, and exist in an environment where moving funds is far easier than it was the last time Schwab went through a rising rate environment. As we’ll discuss shortly, competitors, including another brokerage we recommended last year, have focused on yield in response, and IBKR simply passes nearly all of its interest back to customers.

Meanwhile, management hasn’t looked great over the past year. The huge bet on long-duration bonds can be explained as a hedge against lower rates, which would have further pressured earnings. It can also be seen, somewhat correctly, as an unwise and overzealous acceptance of long-term risk for near-term earnings growth.

With the strength coming out of Q1, we’re not in a rush to sell SCHW. But, admittedly, we are eyeing the door a bit. Schwab simply might not be as good a business as it was, or at least appeared to be, 14 months ago. And if that’s the case, it’s far from guaranteed that the valuation is going to soar past where it traded at the point.

HOOD Rises As Gambling Returns (Right?)

We titled our October pitch for Robinhood HOOD 0.00%↑ “Robinhood Is A Buy (Seriously)”. The “Seriously” was an acknowledgment that many investors saw the business as something not quite credible. As we noted then, a platform not for investment, but for gambling.

But we argued that perception missed the reality. Robinhood did, and does, serve a good number of high-risk traders, but it has a core base of buy-and-hold investors. And it would benefit from the growth in those assets, along with higher rates, which would lead the business to solid bottom-line performance.

Results since then (Q3 and Q4 2023) don’t really seem to support that thesis, or a 74% gain in the stock. Key figures (revenue, monthly active users, Adjusted EBITDA) have flatlined or even declined on a sequential basis. It’s easy to believe that HOOD has simply benefited from the return of crypto optimism and a bull market. That doesn’t seem to be the case, however.

The Robinhood Narrative Changes

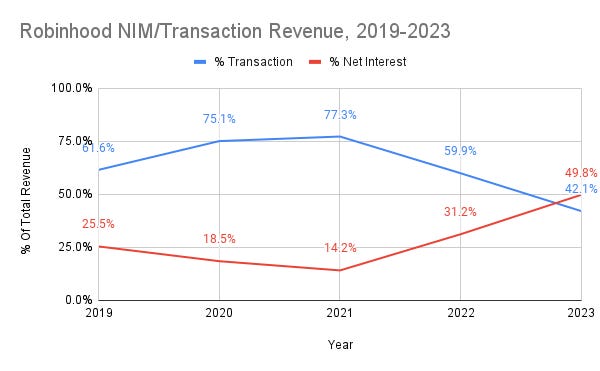

Instead, it appears the narrative around Robinhood has changed — no doubt because the company itself is changing. Simply put, Robinhood seems to be growing up. It’s developed a web-based trading platform, offered an aggressive match for IRAs (Individual Retirement Accounts), launched a cash back credit card, and marketed a high yield on cash sweep (at least for members of Robinhood Gold, which costs $5 per month).

Meanwhile, the importance of trading revenue has diminished. Crypto revenue did spike in Q4, but that increase only totaled ~4% of total revenue. With normalized rates, this business suddenly looks very different:

source: author from Robinhood filings and press releases; figure does not total 100% owing to the presence of “other revenues”.

Investors seem to have noticed. HOOD hit a two-year high last month, after the launch of the credit card. Though it’s pulled back since, the market clearly is treating this like a different, and better, business:

source: Koyfin

The near-term question is whether this holds. It’s possible the narrative around HOOD hasn’t yet changed completely2:

source: Koyfin

The obvious mid- to long-term question is whether all of this works. A 3% match on deposits and then a 5% yield on cash combined with zero-commission trading suggest a reasonably long payback period for some newly acquired customers. (A 5%-plus quarter-over-quarter rise in monthly actives in Q4 does suggest some positive early returns, though crypto optimism in the quarter no doubt re-activated a few small-dollar traders as well).

Q1 and Q2 earnings look particularly key here, because they will provide some evidence both of the cost and success of these efforts. It’s worth remembering that the blue-sky scenario for Robinhood when it went public in July 2021 was not just that it would take share from Schwab and Interactive, but that it would expand into the “financial supermarket” role for the younger generation as it grew older and more wealthy.

The reaction of the market over the past several months is that the blue-sky scenario is back in play. It’s up to chief executive officer Vlad Tenev and his team to keep it in play.

Seneca Foods Still Looks Cheap

When we recommended private-label vegetable canner Seneca Foods SENEA 0.00%↑ last year, the stock on an adjusted basis looked absurdly cheap. The big issue was the company’s accounting, which uses LIFO (last in, first out) instead of FIFO (first in, first out). Amid soaring inflation, Seneca was taking huge LIFO charges which impacted reported earnings and inventory3.

Adjusted for those non-cash charges, SENEA was trading for less than 3x earnings and barely one-third tangible book value. The stock’s removal from major small-cap indices (along with a fairly illiquid market for shares) seemed to have driven a steep decline leaving the stock trading, we argued, well below liquidation value.

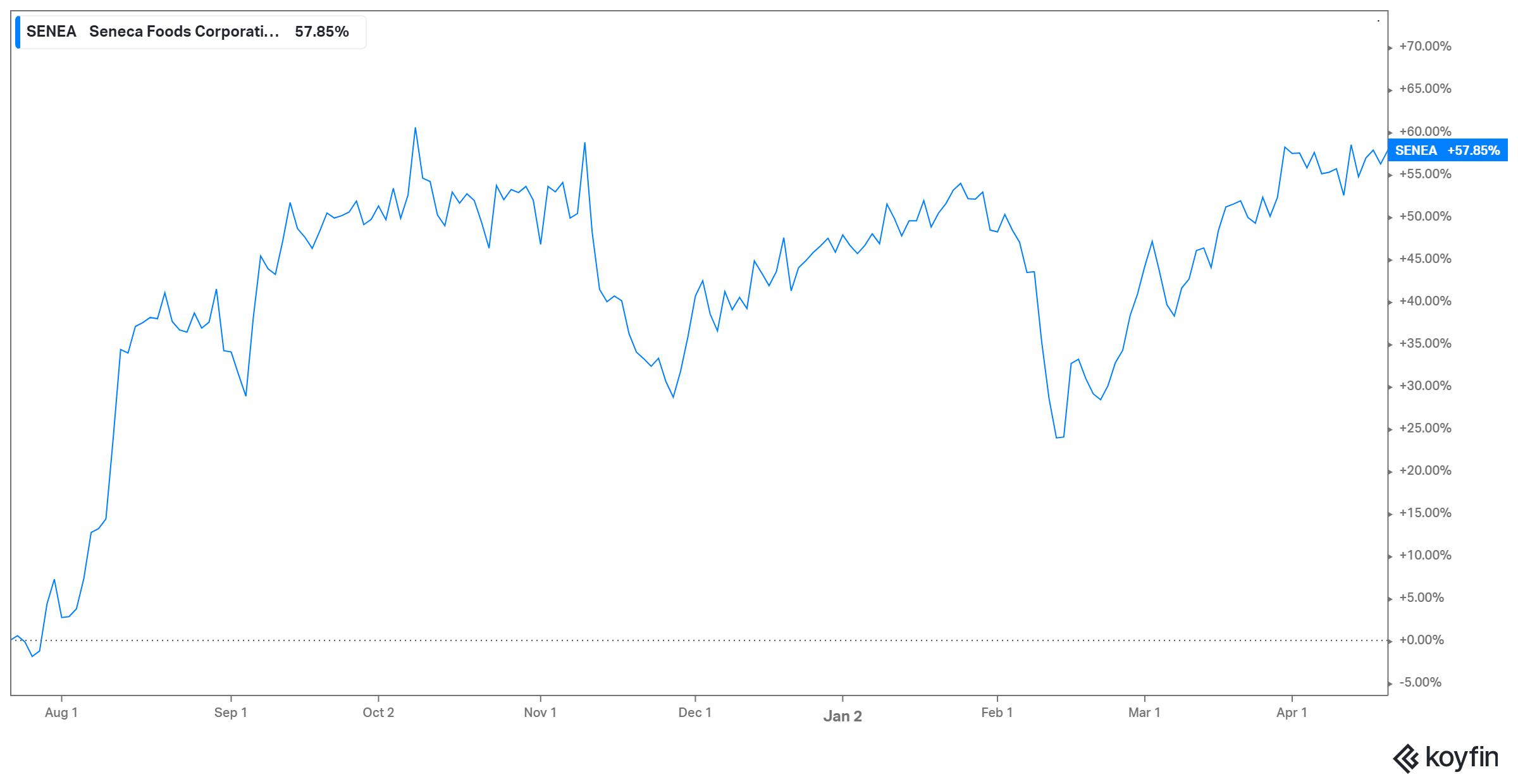

The stock rebounded quickly, and has managed to drift up after that recovery:

source: Koyfin; chart since recommendation on July 23, 2023

An investor can still build a pretty solid case for SENEA on paper. Making the same adjustments for LIFO, tangible book value is $127 per share; SENEA closed Thursday just below $57. Trailing twelve-month EBITDA, again adjusted for the charges, is $196 million, suggesting an EV/EBITDA multiple of about 5.3x. Normalized free cash flow is probably close to $100 million, though LIFO impacts cash tax payments as well4; that’s a P/FCF multiple likely below 5x.

The Value Problem

But there are a couple of issues here. The first is that inflation is stretching the company’s balance sheet. Even adjusted for LIFO, Seneca is carrying more and more inventory, which requires more and more debt. Net debt as of December 30 was $635 million; the figure four years earlier was $211 million. All of that $424 million jump and then some, comes from a $643 million increase in the company’s inventory (again, on a LIFO-adjusted basis). Inventory has doubled in four years, which appears almost entirely due to cost increases rather than volume rises.

This in turn has led to a big jump in interest expense and quite obviously results in lower returns on assets and invested capital. And with volumes actually down sharply this year (and EBITDA declining), there are some worries about the underlying business as well.

The broader issue is that if SENEA is cheap on paper, it’s not clear what that does for shareholders. The company has made some modest moves toward disclosing LIFO impacts in recent communications (though those communications are slim; Seneca does not appear to have held an earnings call since 2012).

In November, it acquired the Green Giant line from B&G Foods BGS 0.00%↑ basically for free: it paid $55.6 million, but also received $52.9 million in inventory. Of course, that’s not exactly a bullish endorsement of the industry by B&G, which was happy to exit for just an ongoing license fee.

Financially, the question is what Seneca can do to turn the recent trend around. It simply has to get back to generating some kind of free cash flow and finding a way to better manage inventory. It hasn’t done so yet: Q4 numbers will look better thanks to seasonality, but even with a repeat of the ~$150M liquidation in Q4 FY23 (ending March), the company is still going to burn for the year.

An acquisition is off the table for a number of reasons. Management has talked up repurchases and has bought back $70 million over the past seven quarters, but capital constraints will force the company away from that strategy if the balance sheet doesn’t improve.

The bigger issue is one we’ve highlighted multiple times over the past twoyears: owning difficult businesses ‘cheap’ is not a strategy that has worked all that well over the past decade and a half. This clearly is a difficult business, as seen in Seneca’s results, B&G’s exit, and even plant closures by Del Monte Foods. In July, it was worth owning that business at an absurdly cheap price. It’s harder now, when the price is simply cheap.

As of this writing, Vince Martin is long SCHW. He may exit his position in the near future.

Disclaimer: The information in this newsletter is not and should not be construed as investment advice. Overlooked Alpha is for information, entertainment purposes only. Contributors are not registered financial advisors and do not purport to tell or recommend which securities customers should buy or sell for themselves. We strive to provide accurate analysis but mistakes and errors do occur. No warranty is made to the accuracy, completeness or correctness of the information provided. The information in the publication may become outdated and there is no obligation to update any such information. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Contributors may hold or acquire securities covered in this publication, and may purchase or sell such securities at any time, including security positions that are inconsistent or contrary to positions mentioned in this publication, all without prior notice to any of the subscribers to this publication. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.

Interestingly, regional banks as a whole, at least based on the SPDR S&P Regional Banking ETF KRE 0.00%↑, have barely recovered at all.

Obviously, this doesn’t necessarily mean Bitcoin and HOOD are directly correlated, with investors treating HOOD as a play on crypto. Both to some degree are simple bets on (and reflections of) broader market sentiment.

Basically, LIFO assumes that the most recent items produced are sold first. Those items are the most expensive in an inflationary environment, which increases cost of goods sold and thus decreases net earnings. It also means that the produced items left in inventory are thus the earliest ones produced — and the cheapest, depressing the recorded value of inventory.

Capex seems to be settling in around $35 million, normalized interest at the current debt load is ~$35-40 million, and cash taxes are probably $15-$20 million, depending on how the accounting shakes out.