Research Notes: Two Big Mergers

Research Notes: Two Big Mergers

We catch up on Primo Water and Six Flags ahead of major tie-ups

Highlights:

Investors appear unimpressed with the all-stock merger between Primo Water and privately-held BlueTriton: PRMW shares have dropped modestly since the announcement.

Some caution makes sense: the tie-up looks great on paper, but there are underlying concerns and risks.

Meanwhile, the merger between Six Flags and Cedar Fun looks attractive and set to complete.

For that deal, concerns are more obvious. But there are echoes of our successful bull call on SIX from 2022. Buying ahead of the merger might still work out.

This week, we update a pair of companies we’ve covered in the past, both of which are executing big all-stock mergers that will make them the leaders in their respective industries.

The Case For Post-Merger PRMW On Paper

On Monday morning, water delivery company Primo Water PRMW 0.00%↑ announced it was merging with privately held BlueTriton, the owner of bottled water brands including Poland Spring, Deer Park, and Ice Mountain. PRMW initially spiked 12% on the news. It finished Tuesday modestly down from where it closed on Friday.

The market’s skepticism toward the deal comes despite what looks like an attractive case for the merger on paper. Pro forma for the tie-up, the business looks relatively cheap, at under 9x EBITDA and in the range of 13x normalized free cash flow1.

The quantitative argument for the stock rests in large part on the appropriateness of those multiples. When we recommended PRMW, we noted the challenge of finding peer comparisons, and that challenge remains — even for the expanded business.

But ~8.5x EBITDA does seem a little too low. BlueTriton was created through the acquisition of Nestle’s North American waters business, for which a pair of private equity firms (Metropoulos & Co. and One Rock Capital Partners) paid $4.3 billion. Disclosures from the merger press release cite 2021 Adjusted EBITDA of $531 million, suggesting Nestle sold for about 8.1x EBITDA. Meanwhile, at Friday’s close, PRMW traded right at 10x 2024 EBITDA guidance, with a high-teens multiple to normalized free cash flow.

Simply using a blended multiple on the Nestle deal and PRMW’s pre-merger valuation suggests the combined business should be trading at just shy of 9x2. But bulls — and executives of both companies — no doubt would argue that the Nestle exit multiple shouldn’t really apply. When Nestle sold the business, it was underperforming significantly, and the entire category was still struggling from pandemic-driven restrictions. Under new ownership, the business has grown Adjusted EBITDA at a 24% annualized rate, which suggests both a recovery in the category and a revitalization of the former Nestle brands.

Meanwhile, the history of PRMW’s own valuation suggests a double-digit multiple. The current Primo Water was created when Cott paid ~15x EBITDA for the former Primo business, which at the time was trading at ~12x. A deal last year to sell Primo’s international business went off at 11x.

Each turn in multiple expansion is worth about 18% to the current PRMW stock price, so if an investor believes the correct multiple is 9.5x or better, the stock is a relatively easy buy here. PRMW shareholders get another ~5% in returns from pre-close dividends3, juicing total expected returns easily past 20%. Coming at the stock from a P/FCF perspective gets to the same sense: if an investor simply believes the business will grow at all post-2025 (and there are some deleveraging benefits that can help), that means the multiple should get closer to the mid-teens, which too suggests mid-20s upside (even before the boost from dividends).

The Argument For The Deal

The numbers, then, suggest the investment case actually is somewhat simple. If an investor likes the deal, PRMW is a buy.

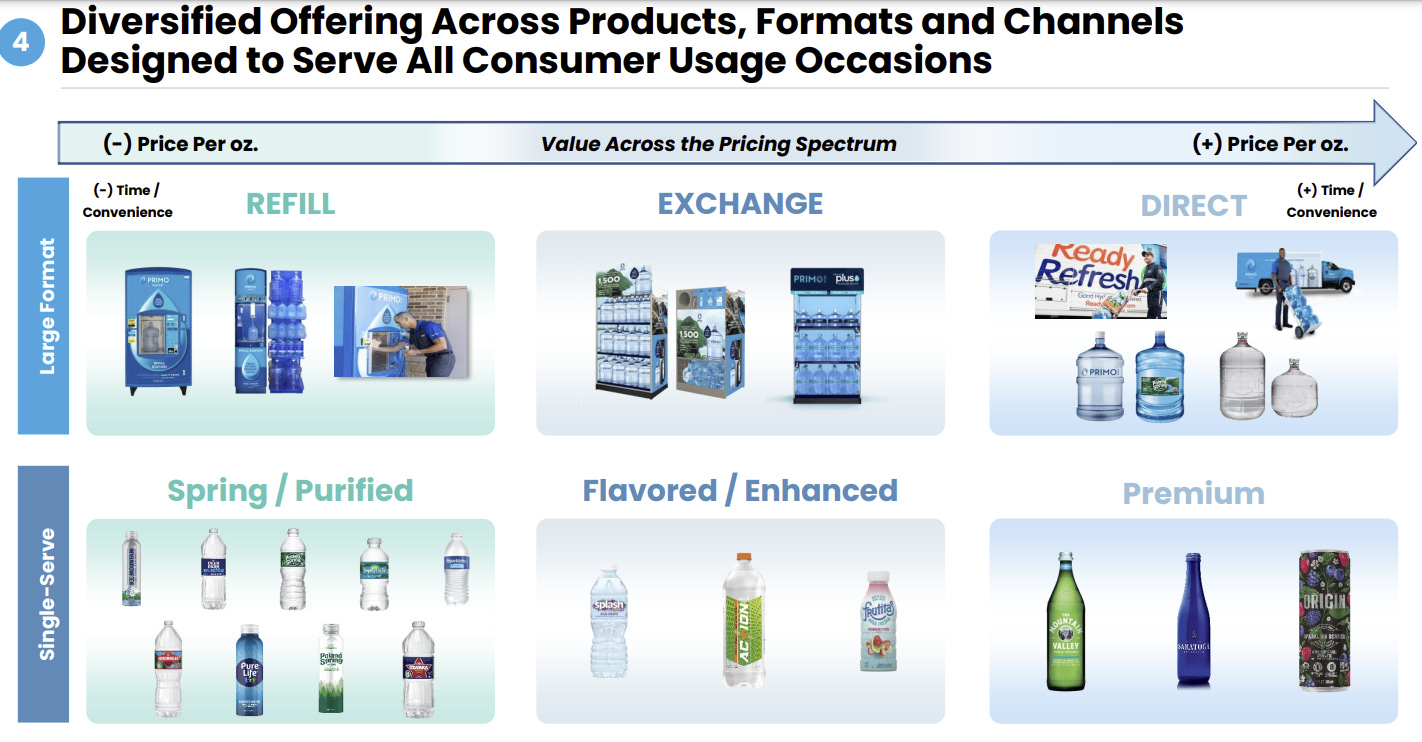

And there is a lot to like here. The tie-up creates a water giant in North America:

source: BlueTriton/Primo merger presentation

Given concerns about U.S. water infrastructure, in particular, that positioning seems wise long-term. Bottled water is already a huge category — about $25 billion in 2023, per data cited in the merger presentation — and it’s one that should post growth above that of the beverage market going forward. The combined company may well have a better go-to-market playbook given the ability to cross-sell across channels, or to use regionally strong BlueTriton brands (Zephyrhills in Florida, Poland Springs in the northeast) for Primo’s legacy home delivery business.

Primo management is staying on to run the combined company, which too seems like a positive. Following an activist effort last year, Primo’s execution under new chief executive officer Robbert Rietbroek seems to have improved notably; full-year guidance was raised after Q1, and PRMW came into last weekend at an 18-year high4. BlueTriton, meanwhile, does seem to have fixed the acquired brands to at least some degree. Chairman and interim CEO Dean Metropoulos cited investments in IT and operations, along with improved efficiency since the merger. The historical data cited in the merger press release suggests BlueTriton improved EBITDA margins by 460 basis points (13.6% to 18.2%) in just three years.

On its face, then, PRMW looks like a relatively strong buy. The valuation is low, both businesses seem to be on an upswing, the long-term outlook is solid and management (Metropoulos will stay on as non-executive chairman) has performed well. It doesn’t require heroic assumptions to project a four-year double here: $2.0 billion in 2028 Adjusted EBITDA (~8% annualized growth off the trailing twelve-month base, pro forma for cost synergies) at a 10x multiple less ~$3.5B in net debt (assuming $1 billion in paydown/share buybacks) should do the trick.

A Lot Can Go Wrong

Yet there are a few concerns in owning PRMW, all of which relate to a simple fact of the merger: PRMW shareholders are now part of the exit strategy for Metropoulos and One Rock.

In that context, the impressive multi-year growth after the Nestle sale might look a little different. Dean Metropoulos cited investments behind the business as improving recent profit margins — but that’s not usually the private equity playbook. Indeed, in Metropoulos’s famous investment, the purchase of Hostess Brands out of bankruptcy, costs and the workforce were slashed soon after the deal.

It’s certainly possible that BlueTriton’s EBITDA margins are at or near a peak. That’s particularly true because packaged foods companies, for instance, were able to use the cover of high inflation to actually improve profit margins in 2023, though that ability has faded of late. And, of course, the P-E owners were highly incentivized to make the business and its profit margins look as good as possible at about this point in the process, which would allow a few years of public market ownership (whether via a merger like this or an initial public offering) before an eventual exit.

If margins are about as good as they’re going to get, that’s an issue going forward, given that BlueTriton accounts for about two-thirds of pre-synergy EBITDA. A business like this that slows to low- to mid-single-digit EBITDA growth (if not worse) isn’t going to see that multiple expansion that underpins the fundamental case.

In the meantime, as even Metropoulos admitted on the conference call, BlueTriton’s P-E owners are probably going to be selling off shares of the combined company. He said the firms would be “careful and measured in how we phase out over the next few years”. Here, too, the Hostess playbook is of interest. Metropoulos took Hostess public via a SPAC (special purpose acquisition company) merger that closed in late 2016; his firm exited their investment just under four years later.

Beyond ownership, there are strategic questions. Creating a giant in water sounds logical on its face, but the two companies aren’t necessarily complementary. Primo’s business and investment case was based in part on taking market share from the single-use market in which BlueTriton mostly plays, with consumer preferences for both price and environmental impact5 a factor. And there’s the question of why Primo needed to dilute (no pun intended) a solid turnaround story driven in part by the efforts of an activist investor last year.

To be sure, these risks are somewhat vague, and perhaps unfair. But Hostess stock was basically dead money in the years after its merger (though it rallied sharply post-2020, and was taken out at $34.25, more than triple its merger price and more than double the level at which Metropoulos exited), and the Primo-BlueTriton tie-up looks quite similar. It wouldn’t be surprising to see history repeat, and in that context, the market’s tepid reaction makes some sense.

The Six Flags-Cedar Fair Tie-Up

Since we recommended shares of Six Flags SIX 0.00%↑ back in August 2022, SIX stock has gained 38%. But the trade took some patience (which I personally didn’t have; I exited at a much smaller profit). More than two-thirds of the rally has come in the last nine trading sessions.

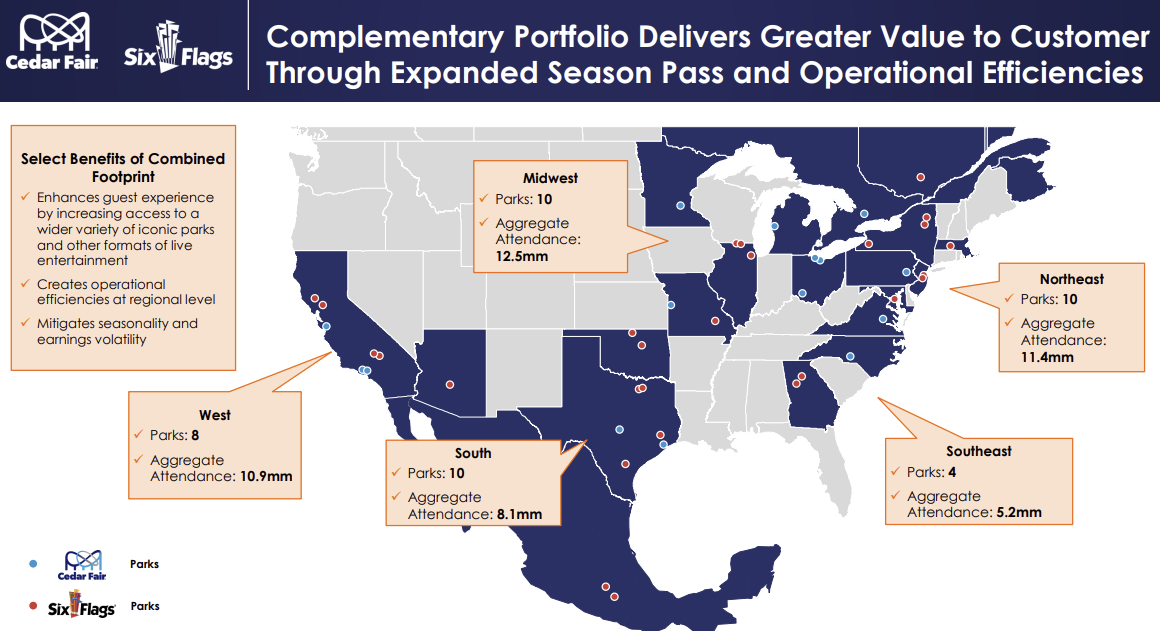

The big news for SIX, of course, is the pending close of the all-stock merger between Six Flags and fellow theme park operator Cedar Fair, L.P. FUN 0.00%↑. The deal will create a nationwide giant with 27 amusement parks, 15 water parks, and multiple other properties:

source: Cedar Fair/Six Flags merger presentation

But, oddly, the rally came into the announcement (which arrived on Tuesday morning), not necessarily after it. Given that the U.S. Department of Justice investigated the merger, the rally makes sense; it’s simply the timing that appears odd.

Whatever the cause, both stocks still look relatively intriguing as they merge into a new company, named Six Flags Entertainment Corporation. Combined, the companies have a market cap of about $5.5 billion; net debt post-Q1 is about $4.75 billion, putting the new Six Flags’ enterprise value at just over $10 billion. At the time of the merger, management guided for Adjusted EBITDA of ~$1.2 billion, implying an EV/EBITDA multiple in the 8.5x range. That’s relatively reasonable given where the stocks have traded of late:

source: Koyfin

And it’s actually quite a discount to where valuations sat before the pandemic:

source: Koyfin

Free cash flow numbers actually look much better. When the merger was announced, the companies cited trailing twelve-month free cash flow (including ~$200 million in synergies) of $830 million. That’s about a 7x multiple, which unsurprisingly is well below pre-pandemic levels as well. Fundamentally, the new company still looks quite cheap, even after the big rally of late.

The ‘Premiumization’ Strategy

Somewhat ironically, those multiples are quite similar to those assigned to SIX when we called it out nearly two years ago. At the time, the stock traded at about 8.5x EV/EBITDA and 11x free cash flow, though the latter multiple dropped toward the 7x range when looking at the late 2010s average. And our case for SIX rested in part on the fact that those multiples, even for a leveraged business, provided a fairly reasonable margin of safety. Meanwhile, upside seemed achievable, as CEO Selim Bassoul rolled out a “premiumization” strategy that would lower attendance and improve pricing. Our thesis was reflected in the title: “It Doesn’t Take Much For This To Get Better”.

At least on the Six Flags side of the merger, that case was vindicated. The premiumization strategy hasn’t really worked as hoped. Bassoul made brief national waves in 2022 by saying his parks had become a “cheap day care center for teenagers”, thanks to discounted season passes. The plan was to get fewer guests who would pay more for a better experience (one that presumably involved many fewer of those teenagers).

The problem is the plan hasn’t been calibrated quite correctly: Six Flags has sharply increased per-capita spend ($61.03 total in 2023 against $42.37 in 2019), but a 32% plunge in attendance has more than offset that improvement. As a result, revenue is down over the five years, and Adjusted EBITDA is off about 12%; Bassoul already has reversed his strategy somewhat.

Yet, to our original point, valuation was such that it didn’t take much to get better. Despite relatively poor execution, SIX has still modestly outperformed the S&P 500 (and crushed the Russell 2000) since our call.

The Case Sounds The Same

An investor can build a case for the ‘new’ Six Flags on similar principles. Valuation is attractive. There is some value in the real estate and the overall asset base using replacement value, which Six Flags (in 2019) estimated at $500 million-plus per park. There still isn’t any significant competition. In most places, Six Flags and Cedar Fair are far and away the only option in town. At 8.5x EBITDA and 7x free cash flow, there’s some protection here in the asset base. Even using perhaps more conservative multiples — that exclude the projection of $80 million in post-merger revenue synergies — EV/EBITDA is ~9x and P/FCF ~7.5x.

New management may help as well. Bassoul is becoming executive chairman of the new company, and I imagine SIX shareholders aren’t terribly upset by that. Shareholders, by a slim margin, voted against executive compensation for 2023. Cedar Fair CEO Richard Zimmerman will keep the same position in the new Six Flags, and recent history suggests that’s a good thing, as Cedar Fair seems to have executed better. Attendance was lower in 2023 than in 2019, by about 4%. But per-capita spend jumped 26% over the period, driving revenue up. Margins have been an issue, admittedly: 2023 Adjusted EBITDA was up less than 5% from 2019 levels.

The question — which is not dissimilar to those asked in 2022 — is precisely what’s going on in these businesses. On a combined basis, trailing twelve-month Adjusted EBITDA is lower than it was in 2019. Many observers have pointed out the weakness in regional theme parks relative to Disney DIS 0.00%↑, whose revenue increased 24% between fiscal 2019 (ending September) and FY23, with operating margins expanding over the period.

Is the weakness in the regionals a sign of changing consumer tastes? Is it execution? Bassoul had an excellent run at Middleby MIDD 0.00%↑, but that was a very different business and strategy (essentially a roll-up of foodservice equipment manufacturers). Or are Cedar Fair and Six Flags, to some extent, post-pandemic losers, with travel spend still being targeted to bigger, longer-distance (Europe, Disney, etc.) trips rather than one-day runs to the nearest theme park?

To be sure, at this point there’s an awful lot of history to suggest that these businesses have some sort of structural problem:

source: Koyfin

Both stocks are well below their 2010s peak, as well as their levels at the end of 20196. Neither business has grown materially during a time when macroeconomic factors would appear favorable.

But, as was the case for SIX in 2022, it doesn’t take that much for this to get better. There are options around real estate monetization, which an activist urged Six Flags to consider last year. It’s possible regional parks benefit from a trade-down in spending away from the bigger, more expensive travel seen over the past three years. Execution no doubt can improve; management of both companies are talking up generative artificial intelligence and self-serve kiosks as a way to lower costs and boost margins. Deleveraging can lower interest expense and increase the equity slice of enterprise value, even if that EV doesn’t move all that much.

More broadly, it does seem like these should be good businesses: insulated from competition, not quite as cyclical as investors might think (in 2009, Six Flags revenue dropped 11% even as the company was going bankrupt; Cedar Fair’s revenue fell only 6%), and serving a very real market of often-enthused customers.

But as far as investors are concerned, they simply haven’t been good businesses. Ten-year total returns in FUN are 47%; in SIX, less than 4%. Many investors will see that history and presume it will continue — and they might be right. Still, this is a deal that makes sense, and if the new Six Flags can find a way to finally improve execution and deliver on its promises, this is a deal that can provide explosive upside. There is a reason why investors have bid SIX and FUN up over the past two weeks, and even after the rally there’s hope more buyers will come along.

As of this writing, Vince Martin has no positions in any securities mentioned.

Disclaimer: The information in this newsletter is not and should not be construed as investment advice. Overlooked Alpha is for information, entertainment purposes only. Contributors are not registered financial advisors and do not purport to tell or recommend which securities customers should buy or sell for themselves. We strive to provide accurate analysis but mistakes and errors do occur. No warranty is made to the accuracy, completeness or correctness of the information provided. The information in the publication may become outdated and there is no obligation to update any such information. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Contributors may hold or acquire securities covered in this publication, and may purchase or sell such securities at any time, including security positions that are inconsistent or contrary to positions mentioned in this publication, all without prior notice to any of the subscribers to this publication. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.

Primo Water has a market cap of $3.56 billion and will own ~43% of the combined company, putting pro forma market cap at $8.3 billion. The companies project net leverage at close (in the first half of 2025) will be 3x, or $4.5 billion, with Adjusted EBITDA currently at $1.5 billion including ~$200M in synergies. That puts pro forma enterprise value at $12.8 billion, and EV/EBITDA at 8.5x.

Capex is guided to 4%-5% of revenue, or about $300 million on a $6B-plus revenue base. Interest is probably close to that, assuming a mid-6% weighted rate (Primo’s current rate is about 6%). Assuming D&A is roughly equal to capex, and using a guided effective tax rate of 26%, tax expense is $240 million-ish, putting FCF around $670 million and the pro forma P/FCF at 12.7x.

43% of the business has a 10x multiple, and 57% gets an 8.1x, suggesting ~8.9x.

PRMW shareholders will probably get three regular payments of 9 cents quarterly (depending on the close, it could be just two), plus a planned 82 cent special dividend.

That essentially is an all-time high, because Cott in 2006 bears no resemblance to its successor company in 2024.

In February 2022, Primo’s own former CEO explained his company’s exit from the single-use market, where it had a small presence, as such: “The increasing effect of one-way single-use plastic bottles in our landfills and waterways have driven us to focus on a more environmentally friendly returnable bottle business.”

Including dividends, FUN does have positive returns since the end of 2019, albeit just 1.2% total.