Fundamentals: Debt That Isn't Debt

Our last article in the series looks at unusual liabilities that matter

This is the fourth article in a series on debt. So far we’ve looked at what debt means for equity investors, what bond prices can tell us, and used Bausch Health BHC 0.00%↑ as a case study. In this final article of the series, we’ll look at liabilities that aren’t actually debt but can have quite similar effects.

The simple definition of debt is that it is a borrowed asset (usually cash) that has to be paid back. In the corporate world, there are liabilities that share the latter half of that description, even if those liabilities aren’t necessarily created by borrowing cash.

For the most part, these liabilities aren’t all that material to valuation. But there are exceptions to that rule, and it’s useful to understand what some of these terms actually mean when seen on a balance sheet.

An Overview Of Non-Debt Liabilities

There are monies that a company will have to pay in the future, even if they are not necessarily debt. Defined-benefit pension plans can run at a deficit (ie, plan assets are less than liabilities), meaning the company is likely going to have to fund its plan at some point.

Contingent consideration represents payments for acquisitions that already have occurred, payments that are based on the acquired business hitting targets negotiated at the time of the acquisition. Companies that once were owned by private equity often have tax receivable agreements, or TRAs, which require the now-public company to reimburse its former owners for tax savings.

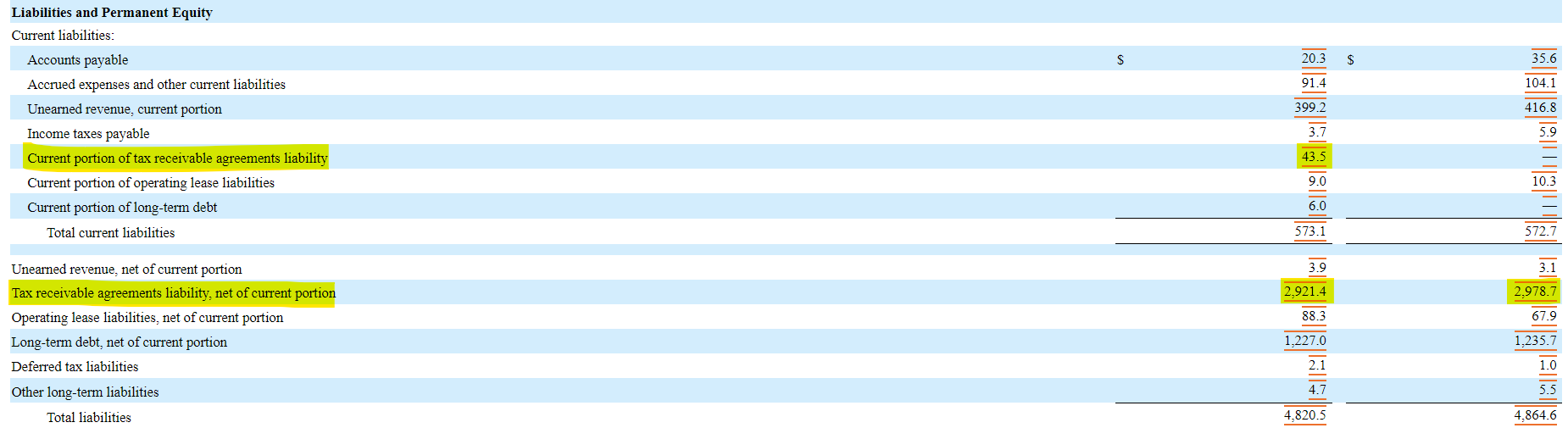

One notable difference between these liabilities and debt, however, is that non-debt liabilities aren’t necessarily fixed. These liabilities do have to appear in financial reports, as seen here in the balance sheet statement from ZoomInfo Technologies ZI 0.00%↑:

source: ZI 10-Q, October 2023 (with author highlighting)

Quite often, these liabilities aren’t fixed, but instead estimated by management. ZoomInfo owes 85% of future tax savings to its former owners — but, obviously, it’s far from certain exactly what those total savings will be. If ZoomInfo’s business falls off a cliff and the company never makes another dollar in profit, the actual TRA liability will be zero. Conversely, if the company generates profits above what management currently expects, ZoomInfo will send far more in TRA payments than it estimates.

And so these non-debt liabilities have to be considered differently than debt, which almost always represents a fixed amount owed with a scheduled maturity. TRA payments can last, in theory, for decades. So too can a pension liability. The line on the balance sheet is a useful estimate — but it’s only an estimate.

What Is Contingent Consideration?

Contingent consideration is money owed to the former owner of a business after an acquisition. The liability usually comes from what are known as “earnouts”, in which the former owners receive additional compensation if the acquired business meets targets under its new ownership.

For instance, a business might sell for $50 million in upfront cash, with another $10 million awarded if that business generates, say, $25 million in revenue in the second year after the acquisition closes. The agreements can be more complicated, with multi-year targets (ie, $25 million in year 2, and $40 million in year 3, with each year sporting its own potential award) or metrics beyond revenue (such as profits, market share, or even the number of customers acquired).

(It is possible in the micro- and small-cap universes to have deferred consideration for an acquisition, where the former owners are owed cash after the deadline closes no matter how the deal performs, but usually it’s too risky to make an acquisition without the ability to immediately fund it.)

When the acquisition closes, the acquirer has to book a liability for contingent consideration. After all, at that point it owes the sellers something of value: essentially, an option on performance of the acquired business. And so the management team of the acquirer will run an estimate for the likelihood the target will be hit, usually using a Monte Carlo simulation, and book a liability accordingly. If the earnout is $10 million and the simulation suggests a 25% chance it will be reached, the liability for contingent consideration should be booked at $2.5 million.

The Value Of Earnouts

Contingent consideration is rarely material to valuation on its own. Even in acquisitions with that feature, the majority of the cost is in the fixed upfront payment: if sellers wanted to maintain the upside optionality in the business, they wouldn’t be sellers in the first place. And of course the total cost of an acquisition (or multiple acquisitions) is usually a small portion of a company’s market capitalization.

But contingent consideration can give valuable insight by providing a ‘true’ account of the performance of acquisitions. The reason is that the calculations underpinning contingent consideration liabilities need to be updated each quarter. The change in liability, then, reflects the most recent assumptions from management about the prospects of the acquired business and the odds that it will hit its earnout targets.

And management has to be completely honest about those assumptions. It’s probably not securities fraud if a chief executive officer says on an earnings call that an acquired business is “performing well”1. “Performing well” can mean almost anything. But it almost certainly is securities fraud2 if a chief financial officer intentionally overstates an earnout liability to create the perception that the acquisition is going according to plan.

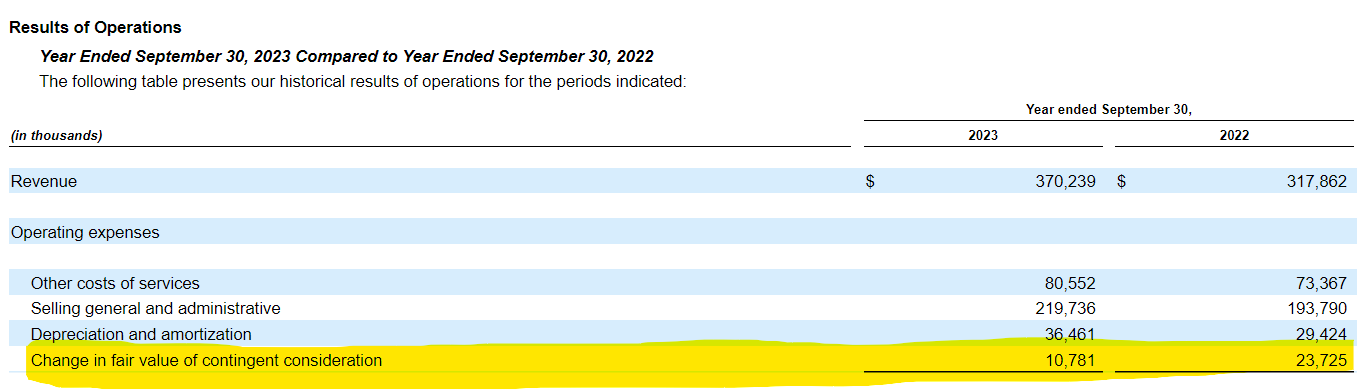

So if a booked liability for contingent consideration goes up, that (perhaps counterintuitively) is good news. Yes, there’s a greater likelihood the company will have to compensate the sellers of the acquired business, but that cost is relatively small. The more important news is that the acquired business is performing well enough that the odds of hitting an earnout have increased. And each quarter, the company will detail in SEC filings how much contingent consideration has changed:

source: i3 Verticals 10-K, fiscal 2023

Last year, we recommended i3 Verticals IIIV 0.00%↑, a hugely acquisitive software company (i3 now has made 49 acquisitions since its founding). And one of the points we made at the time was that rising contingent consideration charges suggested its acquisition strategy was working well.

For i3, the estimate changes seem to be material. Contingent consideration was booked at just $22.8 million at the end of FY22, so the outlook for the acquisitions subject to earnouts has improved noticeably. We can also see in the cash flow statement that in FY22 and FY23, i3 paid more than $37 million in contingent consideration beyond its original estimates:

source: i3 Verticals 10-K, fiscal 2023 click to enlarge

Again, both the original and updated estimates almost certainly were done in good faith. And while there isn’t really a formula to say how important post-acquisition performance is to the stock, common sense says it matters. i3, even up 10% since our recommendation, has a market cap of barely $500 million.

The fact that contingent consideration was revised upward markedly in FY23, and that the company has paid out significantly more in earnouts than it originally estimated, is firm evidence that the acquisition strategy continues to perform well. For a company that makes multiple acquisitions every year, that’s obviously an important piece of information to understand.

Defined-Benefit Pensions

Defined-benefit pension liabilities are rare to see these days at public companies, which have generally tried to push 401(k) plans for worker retirement instead. But we have highlighted Unisys UIS 0.00%↑, whose pension liability is carried at a value greater than the company’s market capitalization. Micro-cap newspaper operator DallasNews DALN 0.00%↑ isn’t quite as extreme a case, but its pension liability is more than 80% of its market capitalization.

Calculating a pension liability is truly an estimate, because so many factors are at play. Actual payments into the fund over time will depend on interest rates (which affect yields for the pension’s bonds), returns in the equity market, and the lifespan of the plan’s participants. One important point to remember is that higher interest rates are actually good news for a pension, since they provide the ability to re-invest maturing bonds at much higher rates. Unisys has estimated that a 100 basis point increase in interest rates lowers its liability by $170 million, an enormous figure given that its market cap is about $340 million at the moment.

Again, it’s rare for pension liabilities to be nearly this material, and in cases like Unisys or DallasNews the issue is discussed quite often on conference calls or even mentioned in investor presentations. For most modern companies, defined benefit plans don’t exist. For older companies, funding isn’t always an issue. IBM IBM 0.00%↑, for instance, said at the end of 2023 its pension was underfunded by $4 billion, but that’s barely 2% of its $175 billion market capitalization.

In the corner cases where pensions matter, using the company estimate as a measure of the liability is probably the simplest method. The data isn’t offered to calculate an independent estimate (we aren’t told specific investments, for instance, or have a sense of the population covered by the pension). And, again, in those cases, management will be aware that investors see the pension as material, and will provide commentary and data on the status of the pension and plans to fix it.

In those scenarios, a pension can be treated much like debt, albeit debt that doesn’t necessarily have a fixed maturity date or a fixed amount. The 10-K should detail mandatory annual contributions, which can be considered somewhat akin to interest. Certainly, they come out of corporate free cash flow. It is possible for earnings to be positive, and free cash flow to be negative, because the pension contribution comes out of the latter but is not included in the former. But, again, in the overwhelming majority of cases, a defined-benefit pension either doesn’t exist or doesn’t really affect the investment case.

Tax Receivable Agreements

For reasons we don’t necessarily need to go into here, a structure known as an “Up-C” can create a deferred tax asset for a company going public3. Unsurprisingly, private equity owners taking their businesses public aren’t keen on leaving the value of that asset for public market shareholders. And so, those companies will execute what is known as a “tax receivable agreement”, in which the former owners are compensated with 85% of the savings created.

The liability can be substantial. In the example above from ZoomInfo, the total TRA liability nears $3 billion. The company currently is worth about $6 billion.

But it’s important to remember that, again, the TRA is just an estimate. More importantly, unlike a pension, a TRA liability doesn’t really need to be “paid back”: money is only owed if the company is making profit that creates tax expense, and even then the company can keep 15% of the savings.

And so a TRA liability really shouldn’t be treated as something akin to debt. That liability is offset by the deferred tax asset created by the Up-C structure (ZoomInfo’s deferred tax asset is currently booked at $3.7 billion). Put another way, a portion of profits are going out the door no matter what: either they are going to federal and state governments or they are going to the former owners. It’s mostly an accounting vagary that requires the latter payments to be booked as a liability, and not the former.

The simplest way to actually account for the TRA is to just value the business on a fully-taxed basis, which most companies will actually do in their adjusted results anyhow. It’s possible, perhaps, to see the TRA (as with earnouts) as a sign of management confidence in the long-term health of the business, but in this case the signal seems much, much weaker.

Most notably, the savings from deferred tax assets can be decades out, and there are many other factors that can affect the liability. For instance, ZoomInfo’s TRA liability came down in 2022 and 2023 in part because the company didn’t make a 2023 payment, but also because a change in Massachusetts state law created lower tax rates (and thus lower taxes on which to generate savings that would then passed along to the former owners).

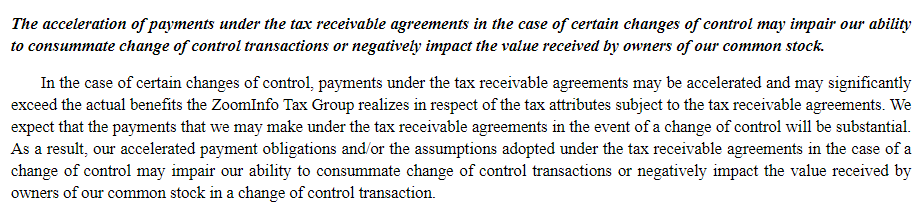

But ZoomInfo does highlight one very important aspect of a TRA. There is a situation in which a TRA acts like debt: when the business is sold. As the company wrote in the most recent 10-K:

source: ZoomInfo 10-K, 2023

If ZoomInfo were to sell itself, it has to reimburse its former owners for the TRA liability. That liability isn’t necessarily a deal-breaker: ZoomInfo writes elsewhere in the 10-K that the TRA payment would be based on the current booked liability, calculated based on a discount rate. Still, that expense might easily be $1 billion or more, a material impediment toward a takeover offer at, say, $9 billion.

In an environment where private equity firms seem happy to own profitable tech firms, ZoomInfo is probably off the market, at least for now. That’s information that obviously is enormously important for investors — but it’s information only understood with an understanding of how something that isn’t debt can, in this case, act quite a bit like debt.

As of this writing, Vince Martin has no positions in any securities mentioned.

Disclaimer: The information in this newsletter is not and should not be construed as investment advice. Overlooked Alpha is for information, entertainment purposes only. Contributors are not registered financial advisors and do not purport to tell or recommend which securities customers should buy or sell for themselves. We strive to provide accurate analysis but mistakes and errors do occur. No warranty is made to the accuracy, completeness or correctness of the information provided. The information in the publication may become outdated and there is no obligation to update any such information. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Contributors may hold or acquire securities covered in this publication, and may purchase or sell such securities at any time, including security positions that are inconsistent or contrary to positions mentioned in this publication, all without prior notice to any of the subscribers to this publication. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.

As Matt Levine would write here, “Not legal advice!”

Again — not legal advice.

Readers can find some details here.