Hindenburg Takes Down A Titan

The rise of activist short sellers and their importance to the market

Editor’s Note: This is the third installment of our new Fundamentals series. If you enjoy this series, let us know in the comments.

The following quotes all come from Twitter, in the wake of the May 2nd short report on Icahn Enterprises IEP 0.00%↑, written by Hindenburg Research. They highlight many of the criticisms of so-called activist short sellers:

Hindenberg research is a nefariously planted "company" by Wallstreet to bash companies and manipulate markets. This is getting published because of $bbby court case.

Ninja technique to make money. First short the stock (evident from the sell off since last 2 weeks) and then drop the report. Then get out on fomo. May be Hindenburg is the face of Financial criminals […] Taking the short position and dropping the report to create the fomo is market manipulation.

How these guys can legally make money off this this is beyond me. Yet the SEC goes after a few retail investors that buy low and sell high. What in the world is the difference here?

It comes down to this - without the report, it’s still trading at $50…Hindenburg is printing money on the short side at the expense of IEP shareholders thanks to a summarized article with a bunch of already public info. A hit piece. Should be ILLEGAL

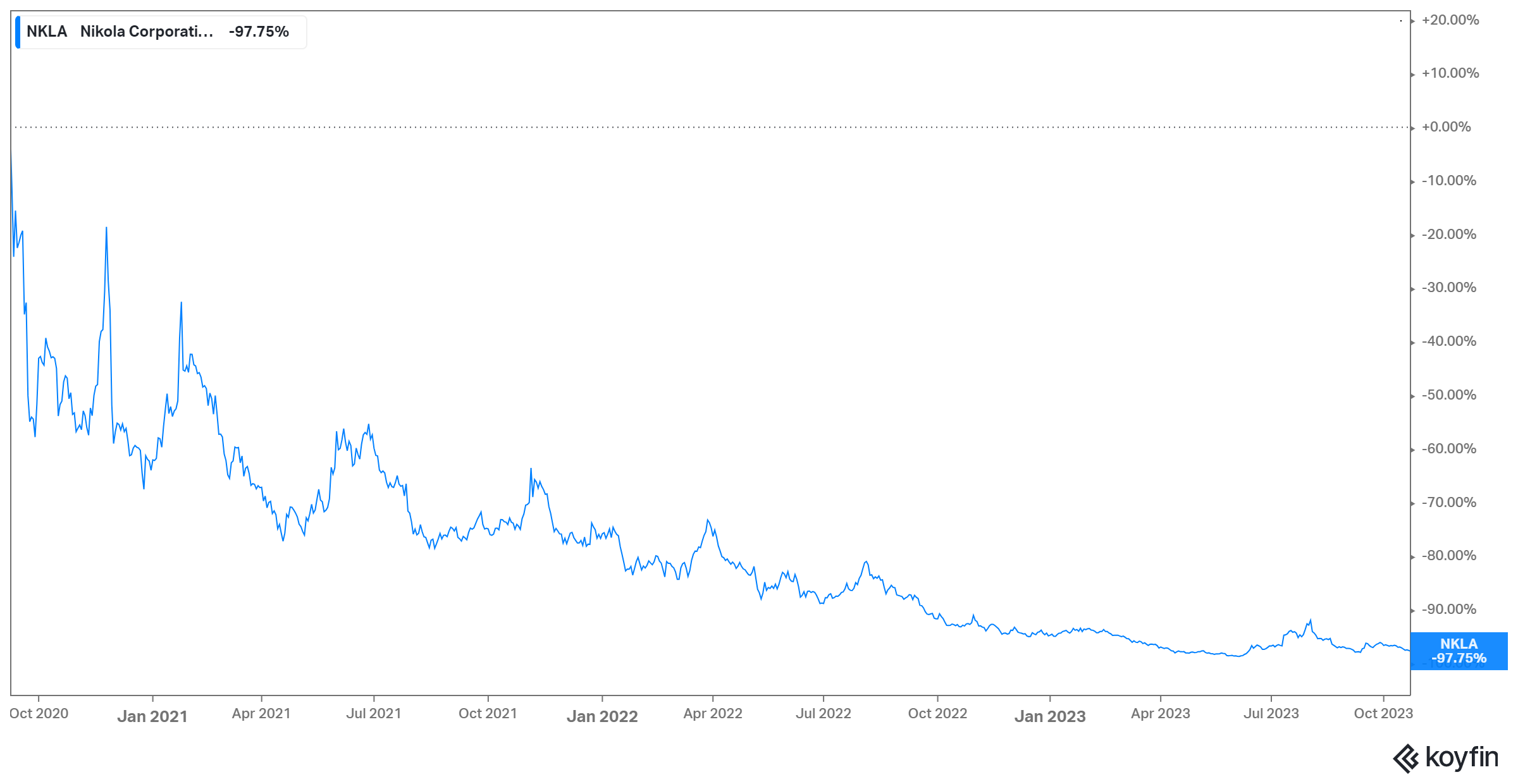

It should be said that Hindenburg is now almost certainly the most well-known (and likely the most successful) activist short seller. The firm’s 2020 report on Nikola revealed significant, long-running deception from the company, deception that eventually led to the imprisonment of Nikola founder Trevor Milton.

Most famously, the company rolled one of its trucks down a hill, while failing to mention that the truck actually wasn’t being propelled:

source: Twitter via Hindenburg Research

Despite the fact that Hindenburg got one right, to many investors, activist shorts don’t seem fair. A blast of negativity comes out of nowhere, with no warning. The stock often moves before shareholders even have time to read the whole report. And those reports almost without exception are incredibly biased. Even if true, they include only the worst information about the business, leaving out many of the company’s positive attributes.

It’s not just investors who are concerned. In late 2021, Bloomberg reported that the U.S. Justice Department had launched a criminal investigation into short seller activities. Commentary from a DOJ official in May suggests results of the probe might arrive any day now. Back in 2017, the then-head of the New York Stock Exchange, referred to short selling more broadly as “kind of icky and un-American”.

But we see it quite differently. Short sellers in general, and activist shorts in particular, serve an important function in the market. And even investors who disagree should respect activist shorts and listen to what they say. As we’ll see, those shorts are often right — and can provide value to all investors even when they’re not.

The Nobility Of The Equity Market

In its highest form, the purpose of the public equity market is to properly allocate capital. Stock prices provide signals to the entire economy that, in theory, should govern investment flows.

Those signals go to the executives of publicly traded-companies: their own stock price might suggest comfort, or dismay, with the direction of their business. Witness, for instance, the market’s recent uncoordinated decision to dozens of companies that “growth at any cost” investment was no longer wise. But the signals also reach competitors, private companies, suppliers, and nearly every other economic participant — including, importantly, the entrepreneurs that provide the next generation of publicly-traded businesses which will serve thousands or even millions of customers.

In this admittedly idealized model, equity investors are rewarded for providing new information to the market1, which makes prices more accurate and, in this telling, capital allocation more efficient2. Because of those accurate prices, the free market functions more efficiently.

Certainly, not everyone agrees with this theory. In practice, there are scams and pumps and dumps and manias and errors. But even in this idealized story, there is a potential problem: how is negative information to be incentivized?

The Role Of The Short Seller

One obvious incentive is that active investors can sell owned equity, avoiding losses faced by fellow shareholders and thus improving their overall returns. For instance, an investor who learned about the rise of GLP-1 agonists early could have exited, say, Hershey, and escaped a larger drawdown.

But the current structure of the equity market provides another incentive: to sell a stock short, by borrowing the stock and selling it into the open market.

This is important. An investor who understood significant flaws in a business or, in certain cases, discovered outright fraud now has a means to profit off that discovered knowledge, improving price discovery in the process. Without short selling, that same investor would almost certainly not buy the stock, but outside of the regular media (whose incentives are not nearly as strong), there would no direct mechanism to get that negative information into the market.

Activist investors like Hindenburg are the bluntest, loudest, participants filling this role. And the role is important. One of the quotes above notes in relation to the Hindeburg/IEP report that “without the report, [IEP is] still trading at $50”. That hypothetical is a worse outcome.

Imagine, for instance, a world in which knowledge of Nikola’s activities was not known for many more years. There would be hundreds of engineers and other employees leaving their jobs (or graduate programs) to move to the company’s headquarters in Arizona, lured by packages of stock that would prove to be close to worthless. Many more billions of dollars of capital, some of it coming directly or indirectly from pension funds (and thus their often middle-class beneficiaries), would have been invested behind a business which almost certainly would have failed at some point regardless3. Learning about that early saves much greater pain down the line.

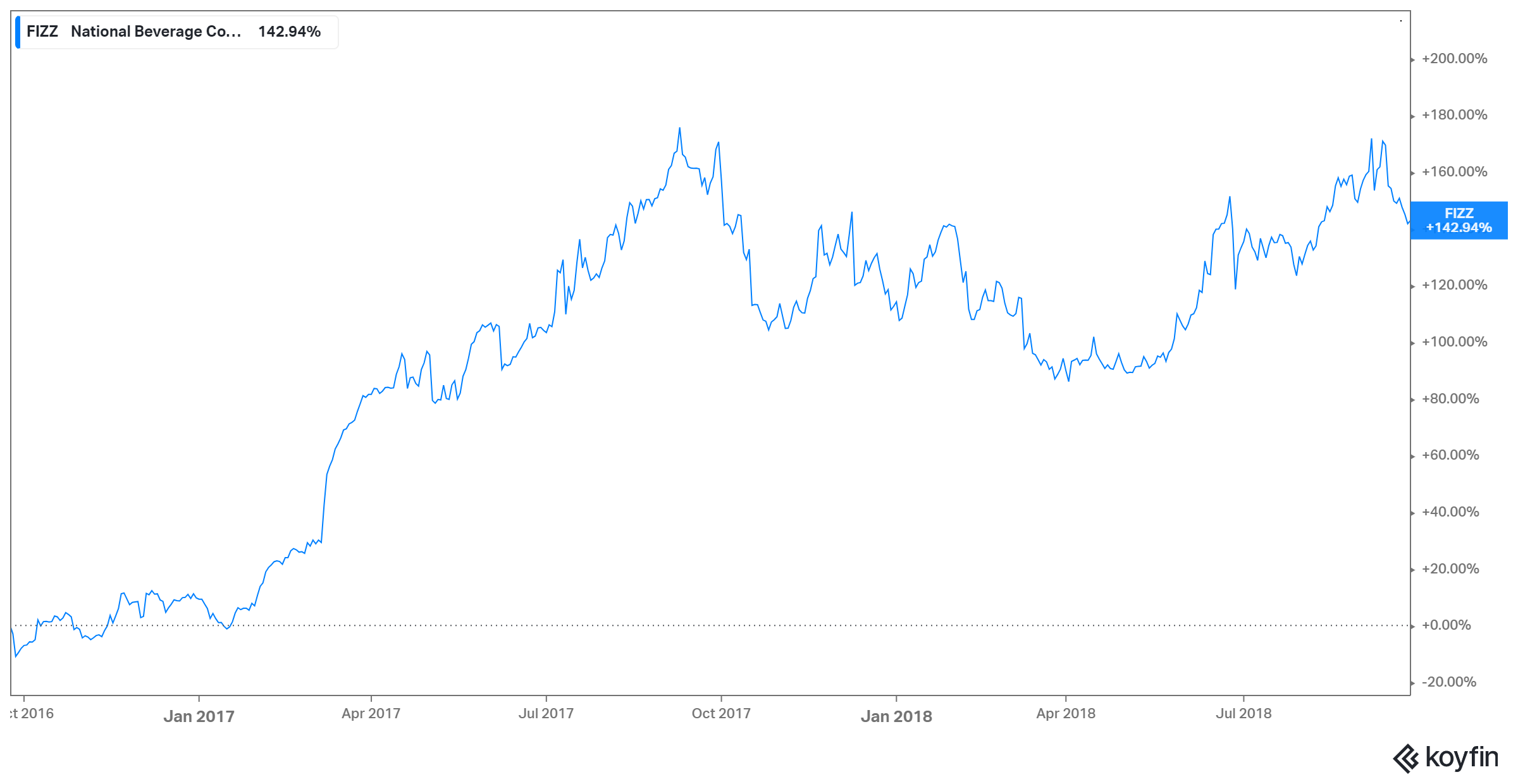

FIZZ Gets Popped

In September 2016, a short-selling outfit named Glaucus Research4 released an activist short report on National Beverage FIZZ 0.00%↑. FIZZ had an interesting backstory. The company was actually created in the mid-1980s to fend off a hostile takeover by an installer of cable systems. Three decades later, founder and chief executive officer Nick Caporella owned roughly three-quarters of the stock, leaving a thin float, and little real interest in the name.

But in the mid-1990s, National Beverage had acquired Winterbrook Corp. out of bankruptcy, and in the process picked up the LaCroix sparkling water brand. LaCroix was well-known in the Midwest, but had a vanishingly small presence outside the region. By the middle of the 2010s, however, its sales were picking up steam as consumers started to abandon diet sodas over health and ingredient concerns. By the time Glaucus took aim at the stock, the FIZZ story was gaining a bit of traction, and the stock had more than doubled in a little over a year.

I read the Glaucus report with great interest because, coincidentally, I had bought FIZZ literally two days earlier. The report was well-written, and the short seller made some good points. Glaucus pointed to exceptionally thin disclosures in National Beverage’s SEC filings, including around compensation for the CEO. (Operations were another issue: the company’s commentary in 10-K filings often boiled down an entire year’s performance to only a couple of sentences.) The firm claimed “inexplicable” operating margins, cited a host of concerns around related-party disclosures and, perhaps most damningly, unearthed testimony in a lawsuit that Caporella had referred to “a little jewel box” with which he would manipulate his company’s earnings.

FIZZ tanked double-digits on the day of the release. Clearly, the market believed the report showed real reason for concern. But if you read the report closely, the airtight case for concern slowly started to fall apart. The “inexplicable” margins (which had begun to expand around 2009) actually made sense when considering that LaCroix had grown largely by word of mouth, rather than through an aggressive marketing campaign.

The case for earnings manipulation didn’t make much sense: Caporella owned three-quarters of the business, meaning a higher stock price didn’t do much other than create paper wealth. (Indeed, Glaucus itself argued that Caporella’s refusal to allow proper due diligence tanked an acquisition by Japan’s Asahi, which itself proved the folly of manipulating a controlled stock.) Perhaps more importantly, National Beverage had barely any analyst coverage: it wasn’t clear what the point of manipulating earnings even would be.

Reacting To A Short

And so, what Glaucus actually had done was create an attractive buying opportunity, both short- and long-term:

source: Koyfin; two-year chart starting week of Glaucus release

There’s a question to how Glaucus created that opportunity. Did the firm find a lawsuit relating to a somewhat illiquid, poorly-covered name with thin disclosures and see that as an opportunity to quickly scalp the stock? Or did it make mistakes precisely because of the thin disclosures and the somewhat titillating, if unproven, allegations in the lawsuit?

From an investing perspective, it’s not a question that matters all that much. Whether or not an investor believes in the role of short sellers, and particularly activist short sellers, they can provide opportunities no matter if they’re right or if they’re wrong.

In this case, I was able to average down on FIZZ, increasing my stake at a more attractive price5. In the case of Hindenburg and Nikola, an investor perhaps would have been upset by an ugly day of trading on September 10, 2020, when the report was released. But listening to the firm would have saved far greater losses from that point on:

source: Koyfin; chart since 9/9/20

Hindenburg and IEP

One important thing to remember when it comes to activist shorts is that reputation is paramount. A poor and/or false report erodes credibility, and it’s credibility that makes the entire process work.

So investors should have listened when Hindenburg came out with its short thesis on IEP on May 2nd. Indeed, many did: IEP dropped 20% on the day of the release.

But, as with NKLA, there was time for investors to get out:

source: Koyfin; chart since May 1

There is one notable difference between IEP and NKLA, however. It’s a key reason why IEP is so reflective of the importance of treating activist shorts with respect: Hindenburg’s report on the stock actually wasn’t that impressive.

To be clear, that’s not to say the report was wrong, or filled with errors. Rather, it was exceptionally simple. The Nikola report in 2020 was a legitimate piece of investigative journalism, with at least one clear source on the inside of the company. In contrast, the IEP report, as one of the Tweets cited at the beginning of this article correctly noted, was “a bunch of already public info[rmation]”.

Indeed, the main points were already public. Hindenburg’s estimate that IEP at the time traded at a 218% premium to its indicative net asset value was based on the NAV figure that Icahn Enterprises itself disclosed in its fourth quarter report. The 53% decline in the investment portfolio between 2014 and 2022 was calculated from data in SEC filings. So was the gap between dividend payments ($1.5 billion) and free cash flow (negative $4.9 billion) over the same period.

In fact, more than seven years earlier, Barron’s writer Andrew Bary made basically the same bear case: Both reports even cited year-to-date losses at CVR Energy CVI 0.00%↑ which had occurred after the most recent publicly-available calculation of indicative NAV. But from the publication of the Barron’s piece to the day before the Hindenburg release, IEP generated total returns of 112%, against 144% for the S&P 500.

All of the gains are gone, and then some. IEP is now -19%, including dividends, since the Barron’s report. Hindenburg had the credibility to move the stock, and it has done so: total returns in IEP are negative 62% since the day before the release.

It’s important to remember that the credibility required to put on the IEP trade only exists because Hindenburg had repeatedly established to the market that it did the work, and did it well. It had repeatedly established that it could, and would, bring new information. It is a bit of an irony, perhaps, that one of its most successful trades came in a report that, essentially, provided no new information at all.

As of this writing, Vince Martin has no positions in any securities mentioned.

Disclaimer: The information in this newsletter is not and should not be construed as investment advice. Overlooked Alpha is for information, entertainment purposes only. Contributors are not registered financial advisors and do not purport to tell or recommend which securities customers should buy or sell for themselves. We strive to provide accurate analysis but mistakes and errors do occur. No warranty is made to the accuracy, completeness or correctness of the information provided. The information in the publication may become outdated and there is no obligation to update any such information. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Contributors may hold or acquire securities covered in this publication, and may purchase or sell such securities at any time, including security positions that are inconsistent or contrary to positions mentioned in this publication, all without prior notice to any of the subscribers to this publication. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.

“New information” here does not require new data or new knowledge; the very act of buying public equity, and thus bidding the price up (or the converse) moves the price. And so the active investor is doing her very tiny part to add to the “wisdom of crowd” and correctly price that equity.

Equity investors in theory are also rewarded for taking on risk, which in turn allows enterprises to undertake projects which are beneficial to society as a whole.

It’s possible that a “fake it until you make it” strategy with Nikola could have succeeded. Other startups have no doubt stretched the truth; the gap between Milton’s conduct and that of other founders who are considered visionaries probably is not that large. Differing outcomes produce very different judgments of the paths to those outcomes.

But, broadly speaking, it’s not good for society as a whole to be funding grandiose projects from companies that are making false claims.

The two principals behind Glaucus amicably parted ways in 2018 and set up two new shops: Blue Orca Capital and Bonitas Research.

As I’ve referenced before, I actually sold the stock soon after, following an insulting interaction with Caporella. That’s a different example of a lesson that clearly applies to this discussion: don’t let your emotions interfere with your investment decision.