Quanex Building Products: A Lower-Risk Play On The Housing Shortage

The housing market, and building products companies, should be just fine going forward. NX stock provides a safer way to play a likely rebound in investor sentiment

Welcome to Overlooked Alpha by Vince Martin and Joe Marwood. Subscribe below to get our best investing ideas direct to your inbox every Sunday morning:

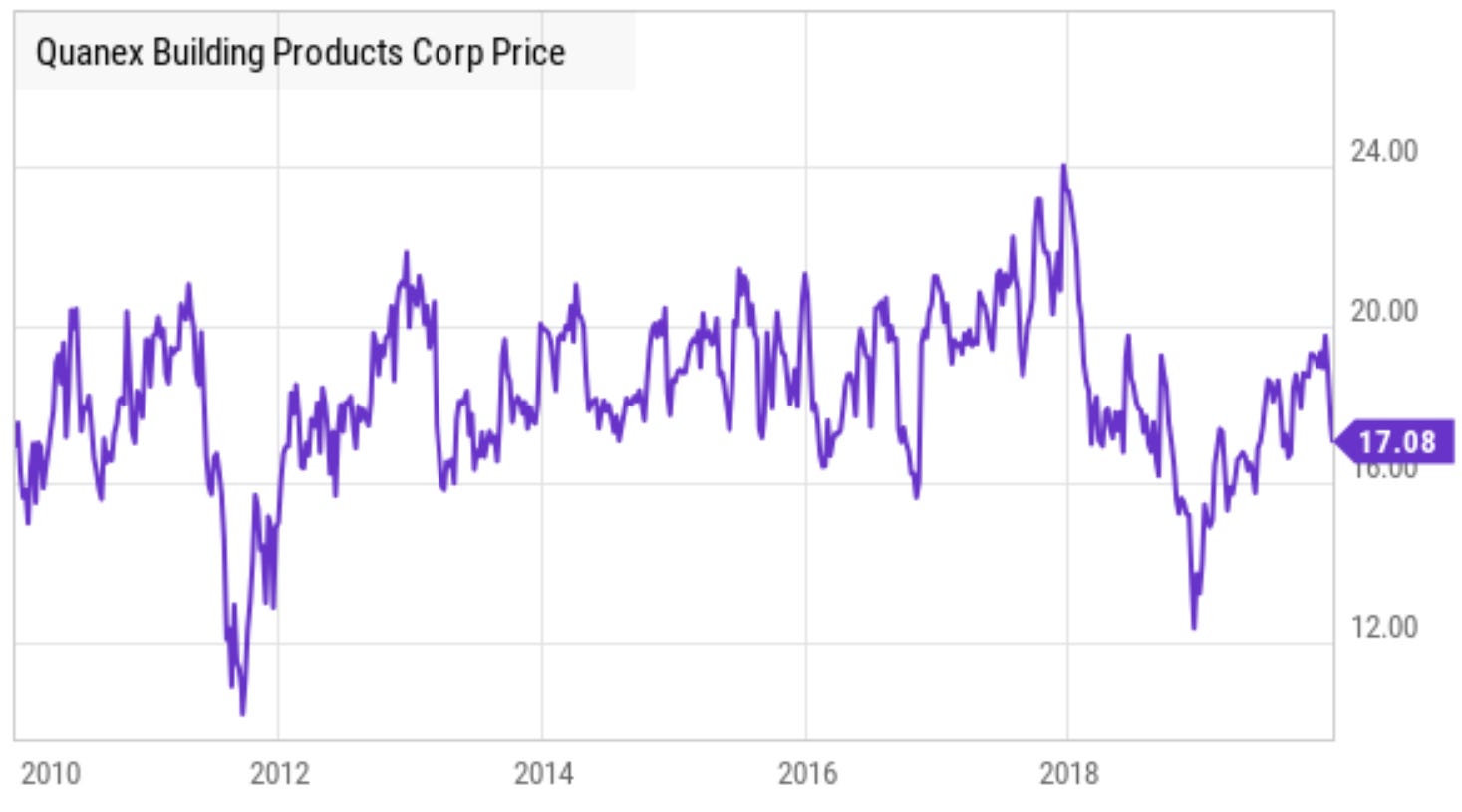

During the 2010s, an investor could have beaten the market by doing deep dives to find the best stocks. Or she could have kept it simple, and bought Quanex Building Products (NX) stock when it hit $16 and sold it when it touched $22:

source: YCharts. NX stock chart from 1/1/2010 to 1/1/2020

It was a trade that I myself put on three separate times toward the end of the run — because it was a trade that made some sense fundamentally as well as technically.

To be honest, Quanex, a manufacturer of components for doors, windows and cabinets, doesn’t have a great business model, a fact which tends to put a lid on valuation, even in a bull market. But at a certain point — and for most of the pre-pandemic decade that point was right about $16 — the business became too cheap. At the right price, the positive attributes of the business were enough to get long.

With sentiment toward both equities and housing (and everything else, it seems) negative at the moment, those positive attributes stand out more now than they did a few years ago. Meanwhile, the building products sector has sold off sharply. Yet there are reasons to think that investors are conflating concerns about housing prices with concerns about the housing industry.

As a result, the sector looks attractive. And while NX hasn’t touched $16 again (it closed Friday at $19.51), and there are many better “go home or go big” plays in the space that have sold off, in this volatile market, NX below $20 looks like one of the best risk-adjusted plays out there.

An Introduction to Quanex

Before the financial crisis, Quanex Corporation had three separate business lines. In 2008, the company sold its vehicular products business (which produced engineered steel bars) to a unit of Gerdau (GGB), and spun off Quanex Building Products. QBP sold its aluminum operations in 2014, leaving a legacy business that produced spacers (which separate the panes of glass in a window), vinyl and composite extrusion profiles (custom-manufactured shapes), screens, and precision-formed wood and metal products.

In 2015, Quanex added on UK-based HL Plastics to boost its business in Europe. Later that year, the company moved into the cabinet space through its acquisition of Woodcraft for $246 million in cash. That deal moved the company’s pro forma net leverage to nearly 3x Adjusted EBITDA. Save for a tiny divestiture of a wood flooring plant in 2017 (for less than $2 million), the Woodcraft purchase ended Quanex’s decade-long effort to remake itself.

To at least some extent, the strategy hasn’t been that successful. NX stock has badly underperformed, gaining less than 9% total over the past decade. 10-year annualized returns even including dividends (NX currently yields 1.6%) sit right at 2%, against 10%-plus for the Russell 2000.

One core reason for the underperformance has been that the Woodcraft acquisition has not worked out, to put it mildly. Again, Quanex paid $246 million; in FY21 (ending October), the North American Cabinet Components segment — which is Woodcraft — generated $14.2 million in EBITDA. That’s less than half the EBITDA expected at the time; margins have gone from a planned 13% to under 6%.

Good News and Bad News

There’s very much a good news/bad news split to Quanex’s business model, across its three segments (the legacy fenestration1 business, as it’s known, reports in North America and Europe).

For the window component business as a whole, switching costs are relatively high. A customer that moves to a different supplier has to retool its manufacturing lines to do so. This is good news in the sense that revenue tends to be relatively stable. That stability is also bad news. It’s difficult to lose market share, but difficult to gain it as well.

Over the years, per management commentary (and market data figures from 10-K filings), Quanex has gained a bit of share, but for the most part revenue in the North American Fenestration and European Fenestration segments tracks the window shipment market.

Those businesses accounted for 90% of segment-level profit in FY21; if end markets turn south, Quanex’s revenue does the same. Obviously, with interest rate hikes on the horizon, investors are fearful of precisely this kind of decline, one reason why NX stock has dropped 24% just since Dec. 29.

The same sense holds in the individual regions. In Europe, economic worries are probably more pronounced than in the U.S., given post-Brexit struggles in the key U.K. market. But environmental tailwinds — notably around the requirement for energy-efficient windows — are stronger, and competition is lighter. Indeed, margins on the Continent have run higher (360 bps in FY19, up to 690 bps in FY21, with the segment hitting nearly 20%).

But in the U.S., there is some opportunity for margin expansion left. Management has admitted repeatedly in recent quarters that the goal overseas is simply to protect what margins there are. In the U.S., there is still hope, in a more normalized environment, to get to ~15% from the low-13% range of the past three years.

In the cabinet business, the bad news is the cabinet business. Again, Woodcraft has been a huge disappointment, and despite efforts from management the news hasn’t gotten much better. Adjusted EBITDA margins have been below 6% in each of the last three years. FY21 revenue was modestly below the figure four years earlier. In late 2019, one analyst even asked if Quanex would consider exiting the business altogether.

A key part of the problem has been a shift in the end market. (Here, too, Quanex is largely at the mercy of the end consumer.) Semi-custom cabinets — which offer some level of customization, but aren’t custom and/or high-end options — rapidly ceded share to lower-priced ‘stock’ models. Quanex management attributed this in part to intense pricing competition from big-box stores.

Woodcraft’s customers have taken a hit as a result. One even exited the business altogether in late 2019, which reduced Quanex’s annualized revenue by $11 to $12 million, about 5% of segment sales. Yet even as that shift, per Quanex management, has stabilized in recent years, and even as the pandemic disrupted the Asian-based supply chains of many bargain-basement manufacturers, results simply haven’t improved.

The good news in the cabinet business, however, is that it doesn’t matter all that much. Again, it accounts for ~10% of segment-level EBITDA, and given capex requirements, an even smaller proportion of free cash flow.

What Goes Wrong

Net/net, as far as businesses go, Quanex isn’t the best one in the market, admittedly. Much of the company’s performance is driven by factors far beyond its control — which, again, hardly seems like a good thing at the moment.

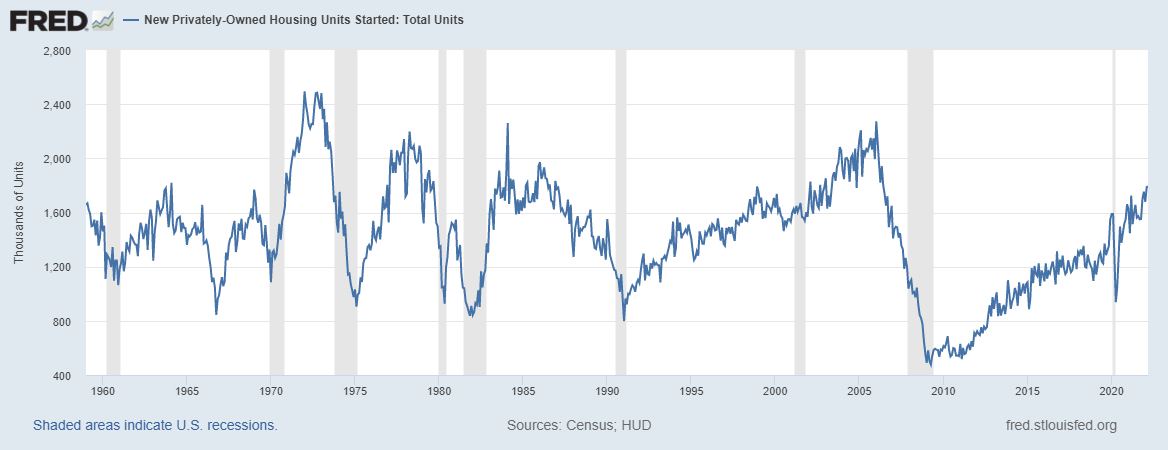

Housing starts have steadily risen in recent years:

source: St. Louis Fed

But higher interest rates threaten new construction. Quanex’s fenestration business tilts more toward repair & remodel, but new construction remains a key catalyst. If that turns, window shipments turn south, and so does Quanex’s revenue.

Interest rates also factor into financing for R&R — and raise the specter of a recession, which will further pressure spending. Classic cyclical worries thus are a big problem here, and, again, likely a key factor in the recent sell-off for NX and its sector.

Inflation provides another problem. In North America, most Quanex fenestration sales have pass-through pricing based on a commodity index. But there is a lag in that business and in cabinets, and in Europe Quanex has take pricing itself. It’s been able to do so to this point, but a “stagflation” environment offers a potential double whammy.

Quanex is dealing with labor inflation as well: as of Q3 FY21, wages alone had risen $5.1 million on an annualized basis. In June of last year, the company estimated normalized SG&A at $90 million to $100 million; FY22 guidance anticipates $115 million to $120 million.

There’s another potential worry here. Quanex’s profits in fenestration actually declined 8%-plus between FY16 and FY19. EBITDA growth only arrived in FY21, with guidance for a further increase (6.5%-10.4%) in FY22. Quanex chief executive officer George Wilson himself on the Q1 FY21 call gave one reason why that might have happened:

We also believe demand in Europe and the UK is being favorably impacted by the continued shift of the discretionary income away from travel and leisure activities into home improvement projects.

In other words, Quanex might actually be a pandemic winner. Even if a recession doesn’t arrive, normalized R&R spending plus lower housing starts could in theory result in a return to pre-pandemic revenue and profits. Quanex is guiding for $135 million to $140 million in FY22 Adjusted EBITDA, which translates to $75-$80 million in normalized free cash flow. FY19 Adjusted EBITDA was just $103 million, which in turn suggests normalized FCF closer to $50 million.

The final worry is that known to every value investor: capital allocation. As noted, Quanex was almost 3x leveraged when the Woodcraft acquisition closed. Net leverage is nearly zero at this point. Guidance suggests Quanex should end the year with $35 million-plus in net cash. (Q1 sees free cash flow burn, owing to inventory buildup.)

Quanex doesn’t sound entirely sure what to do with the capital. The company does have a $75 million share repurchase authorization, though Wilson says he’s concerned about the impact of buybacks on a relatively small float. On and off, Quanex has floated M&A; Wilson sounded skeptical a few years ago, more constructive last year, and then said after Q1 that “the deal pipeline in general slowed down a little.”

It does sound like Wilson is taking a sound approach to M&A; there’s been no hint (at least publicly) of a Woodcraft-style deal. And there is room for Quanex to raise its dividend if need be, though for now some cash is going to go to repurchase activity.

But, again, every value investor understands the risk a seemingly solid balance sheet can create. The Woodcraft acquisition itself provides a cautionary tale.

Taking A Deep Breath

Broadly speaking, the risk is that Quanex is a cyclical potentially at the end of the cycle; and, failing that, a value trap.

As always, the risks need to be understood. But taking the long view, there’s a strong chance that the market is overreacting toward the stock, and the sector. And, indeed, the sector has been hammered of late. The iShares U.S. Home Construction ETF (ITB) does include homebuilders, but also a heavy dose of suppliers, and it’s sold off sharply this year:

Again, the clear worry is that interest rate hikes are going to pressure demand. And while there might be some truth to that in the coming quarters, the long-term case for U.S. housing still looks solid for one simple reason: there’s still a significant housing shortage in the U.S. By one estimate, the country needs more than 3 million new homes to meet current demand (the story is much the same in the U.K.)

Meanwhile, if buyers can’t find new homes — or can’t afford to buy existing ones — the next alternative is to improve their existing residences. It’s too optimistic to believe that window demand is going to rise no matter what, it’s similarly far too pessimistic to believe that the industry is headed for looming disaster. Right now, the pessimists clearly are driving NX stock.

The focus on rates and macro factors also ignores a pretty key issue: while demand might have been higher than usual it recent years, it’s not like Quanex was dealing with some wholly beneficial environment in ~18 months following the pandemic. Inflation has hit margins, with even pass-through contracts seeing a lag. Backlog at Quanex’s customers worldwide remains high, in large part because labor has provided a bottleneck to installation. At one point last year, Quanex itself had 400 open positions — a total equivalent to about 10% of its workforce. More recently, absenteeism due to the Omicron variant caused problems.

Quanex is looking to ameliorate its labor pressures by increasing automation in its manufacturing processes. But production of the automation equipment itself has been slowed by the same supply chain and labor headwinds, along with demand from so many companies looking to that equipment to manage their own near-term challenges.

There are risks to Quanex from a return to normalcy (in the housing market and potentially elsewhere), but there are potential rewards as well.

And while Quanex’s results are tied to end markets, there are some potential catalysts as well. Labor pressure has helped drive some growth, particularly in window screens, since window manufacturers are looking to narrow their focus and thus are outsourcing that portion of the business. The threat of long-distance supply chains has been laid bare since the pandemic, and could provide some hope for reversing the tide in the cabinet business.

A new automation technique can benefit so-called “warm edge spacers” used in high-end windows, providing incremental high-margin revenue. Quanex is adding capacity in the UK and Germany; there’s room for more geographic expansion of the screen business in the U.S. The cabinet business can’t get much worse. And, again, even stabilization of input cost inflation at this point is a benefit to margins across the company, as pricing catches up.

The next few quarters are going to be choppy, but that alone doesn’t mean profits are heading back to pre-pandemic levels. After all, the last few quarters were choppy, too. Quanex has managed through nicely, and there are reasons to believe the company can do the same going forward.

Valuation, A Sale, and Alternatives

One of the reasons that NX stayed range-bound before the pandemic was that the business didn’t move much. That could be seen as a risk — the company couldn’t benefit from a long macroeconomic expansion — but it also highlights the case for the stock going forward. Over time, window market demand is going to grow slowly. That’s bad news, relatively speaking, in a bull market. It’s probably good news in a bearish one.

And at this point, low growth implies significant upside. Looking to FY22 guidance, NX trades at barely 5x EBITDA and ~9x normalized free cash flow. Neither figure includes the reversal of working capital that should drive realized FCF over the next three quarters; that cash alone accounts for more than 10% of the current market capitalization.

At some point, too, the ~stable trajectory and deleveraged balance sheet may make NX an intriguing P-E target. Clayton, Dubilier & Rice went into the space for more than $2 billion in early 2018, buying Ply Gem and Atrium Windows & Doors in separate transactions.

To be sure, the case here might perhaps support going after more leveraged, more risky plays in the sector. From a macro perspective, such a trade seems strong long-term, if potentially early. But from here, NX offers a lower-risk alternative. Yet the steep sell-off (YTD performance is not materially worse than ITB) suggests the market isn’t pricing it as such. Particularly at this point in the sell-off (one which really doesn’t look like it’s near an end), I’d rather try and time the bottom with NX than another play in the space. (It still looks too early to time the bottom at all, but that’s a different article.)

Simply put, NX stock is as cheap as it’s been — ever. (Shares historically bottomed out around 7x EBITDA.) And for more than a decade, investors have stepped in when the stock got cheap enough. The macro environment probably is better than feared going forward, and not quite as good as believed looking backward. Cash is going to come gushing in over the next couple of quarters, simply because it will take at least that long for customers to work through their backlogs. And there are modest catalysts for upside on the horizon.

It’s an attractive combination. When the market rebounds, NX should be able to do the same. The biggest risk might be when that rebound actually arrives.

Vince Martin has no positions in any securities mentioned, but may initiate a position in NX stock this week.

Tickers mentioned: NX 0.00%↑

Disclaimer: The information in this newsletter is not and should not be construed as investment advice. Overlooked Alpha is for information, entertainment purposes only. Contributors are not registered financial advisors and do not purport to tell or recommend which securities customers should buy or sell for themselves. We strive to provide accurate analysis but mistakes and errors do occur. No warranty is made to the accuracy, completeness or correctness of the information provided. The information in the publication may become outdated and there is no obligation to update any such information. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Contributors may hold or acquire securities covered in this publication, and may purchase or sell such securities at any time, including security positions that are inconsistent or contrary to positions mentioned in this publication, all without prior notice to any of the subscribers to this publication. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.

Fenestration literally refers to the openings in a building.