Research Notes: Still-Good Ideas

We return to recommendations from the past that look attractive in the present

Highlights:

Our performance remains solid, particularly given constraints and comparison to the top-performing index.

NATH and COHR have performed very differently, but each story still looks attractive going forward.

CLFD unfortunately has been a disaster — but with a fortress balance sheet and government help coming, the long-term case at the lows seems intriguing.

ABM has done basically nothing in the 16 months since recommendation, but patience may still be rewarded. ADV has rallied nicely, but risk-loving investors may see more upside ahead.

Since our launch on March 31, 2022, we’ve covered 240 stocks, and made 74 directional picks in our deep dives. To this point, our performance looks solid, if not spectacular. Our average return of +6.6% is about in line with the S&P 500 (when comparing each individual recommendation to the index’s performance from the time of publication). On an annualized basis, we’ve generated about 10 percentage points of alpha. All of that has come from the short side; our long ideas have modestly missed the index.

But as we’ve written before, that performance is much better than it appears given the constraints of writing a newsletter. Generating ~50 ideas a year is not easy. Publishing on Sundays also creates some friction. For instance, Robinhood HOOD 0.00%↑, the subject of last Sunday’s deep dive, gained more than 3% between when we decided to make it the focus of that piece and Monday’s open.

And while we track performance, we don’t run a model portfolio. The spreadsheet exists to provide a check on our performance, not a granular reproduction of an investor’s success following our recommendations. We have closed out a good number of positions, but that is not the same as aggressively maximizing the returns we show to readers.

Notably, we have to this point compared our performance to the S&P 500. Starting soon, we’ll add a comparison to the Russell 2000, which provides a more accurate benchmark given our focus on small and mid cap stocks. All told, we take pride in our performance. At the same time we continue to work toward improving it.

This week, we’re going to take a closer look at some of those past ideas. We’ll start with one of our first, and best-performing.

Nathan’s Famous Is Still A Buy

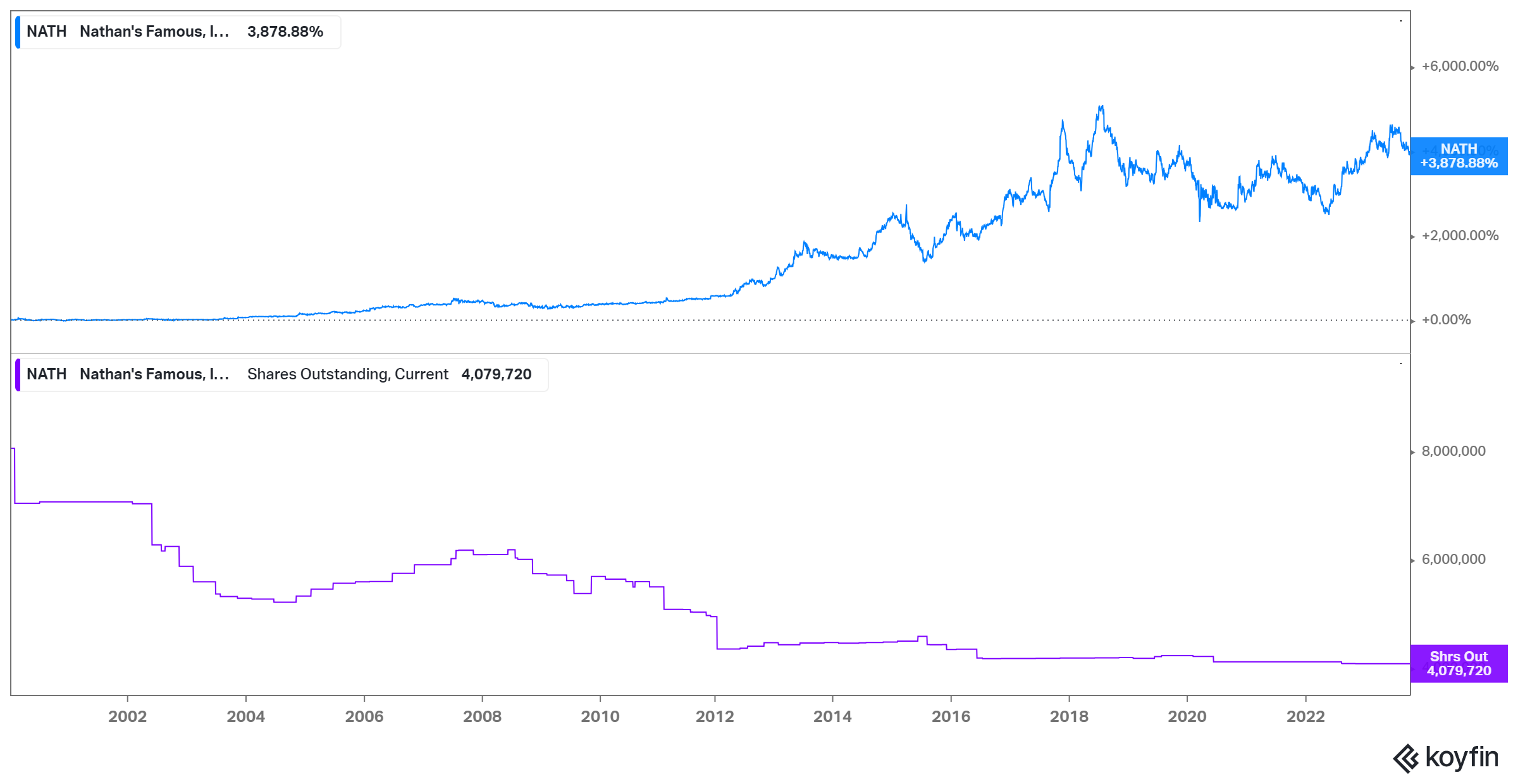

We pretty much bottom-ticked Nathan’s Famous NATH 0.00%↑ last May. Amid a rout in small-caps, the stock traded at a five-year low. Including dividends, NATH has returned 51% since.

That performance is good — but not that long ago, it was better. NATH is down 13% since the end of July. As was the case last year, another rout in small-caps appears to be playing a role. The company’s fiscal Q1 report at the beginning of August led to some selling, but to our eye looks fine. Adjusted EBITDA was basically flat. Excluding two small yet lumpy factors (cancellation payments in the restaurant business and stock-based comp) it would have risen roughly 2% year-over-year on a difficult comparison.

All told, Nathan’s Famous is performing well in an inflationary environment. Yet after the sell-off, valuation once again has come in. On a trailing twelve-month basis, NATH trades at 14.1x earnings per share and 9.2x EV/EBITDA — basically the same multiples assigned 17 months ago. There are still three quarters ahead in which interest savings from a March bond repurchase (which added ~$0.09 to Q1 FY24 EPS) will contribute to year-over-year EPS growth1.

When we last updated NATH, in June of this year, we argued that despite the higher price the story was still much the same as it had been when we first pitched the name. With the stock pulling back, the story feels even more similar now. If anything, the story might be better. The balance sheet is less leveraged (2x-plus then, just 1.3x now), which opens up options for a management team that has been aggressive, and successful, in terms of capital allocation.

source: Koyfin. chart since 1/1/2000

That management team is getting older as well. Most notably, executive chairman Howard Korber, who owns 24% of the company, is 74. Two other 6%-plus holders are 68 and 70, respectively. The balance sheet is as clean as it’s been in at least a decade, and with a licensing business that generates ~three-quarters of profit, this is a good fit for a go-private at some point.

The price is obviously materially higher than it was in May. But lower debt and higher earnings are the cause of the increase — not higher multiples. We still like NATH as an attractive long, and it remains of one of my largest positions.

Coherent Makes A Deal

For Coherent COHR 0.00%↑, too, the story is much the same as it was when we first recommended it. The difference here is that the price is about the same: COHR has gained only 3.4% in the nearly six months since publication.

Initially, the market jumped on to the same thesis we had: seeing Coherent as a winner in growth markets like electric vehicles and artificial intelligence. But ugly guidance after fiscal Q4 results in August sent the stock tumbling back down.

That selling looks like the market focusing on short-term, and somewhat cyclical, factors over a long-term opportunity. As we noted on Twitter this week, Coherent strengthened that opportunity with a $1 billion sale of a 25% stake in its silicon carbide business. The sale not only values the remaining ownership at ~$3 billion (Coherent’s enterprise value as a whole is barely $11 billion), but funds the SiC buildout and provides two built-in customers for wafers going forward.

It may take some time for this opportunity to play out, admittedly. On its face, COHR doesn’t look cheap. Just below $35, shares trade at 28x the midpoint of FY24 EPS guidance of $1.00-$1.50. That guidance compares very unfavorably to adjusted EPS of $3 in FY23, and $3.72 the year before. Leverage is a concern as well: net leverage was 2.9x EBITDA at the end of FY23, a ratio that should move closer to ~4x as fiscal 2024 rolls on.

There are risks, certainly, but they appear worth taking. Indeed, I bought shares on the news this week, and I wouldn’t be surprised to see a steady melt-up in the coming weeks. It’s easy to see why the market got spooked by Q4 results, but given the long-term opportunity it’s also easy to see why the market might return to the recent optimism that sent the stock above $50.