Fundamentals: Short Selling And Short Squeezes

A primer on the who, why, and how of selling short

Short selling has long had a reputation for being distasteful, or even manipulative. An opinion piece from Reuters in 2008 — as global markets were plunging amid the financial crisis — noted that “short sellers have been the villain for 400 years”.

Joseph P. Kennedy, the father of John F. Kennedy, was said to have made his fortune by selling short ahead of the Crash of 1929. It’s not clear whether that, or his alleged bootlegging, was supposed to be more damning. Even in 2017, at a time when U.S. stocks were doing quite well, then then-head of the New York Stock Exchange said that “it feels kind of icky and un-American, betting against a company.”

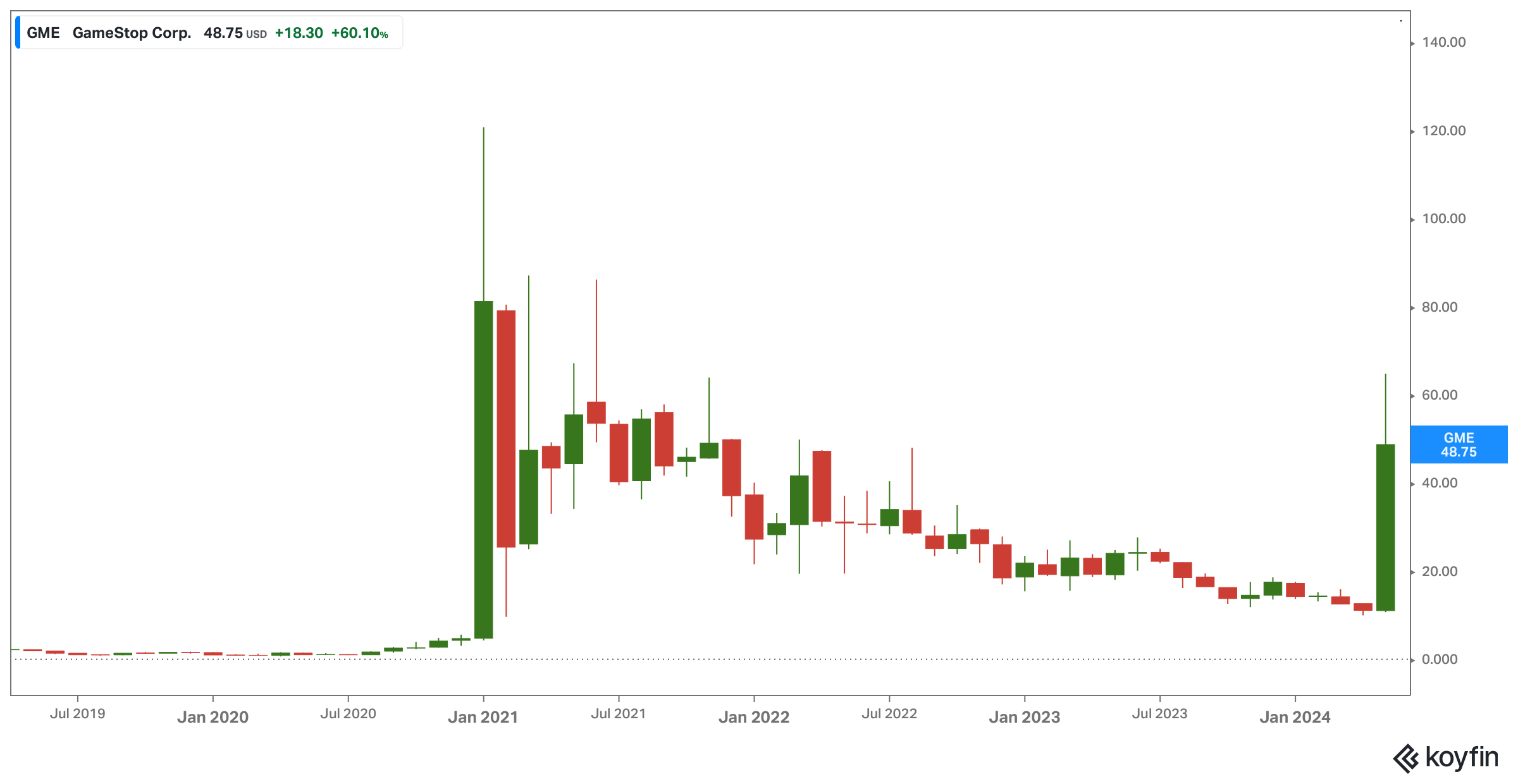

But it’s almost certain that at no point in market history have short sellers received as much scrutiny, and indeed as much attention, as they have over the past few years. The incredible rise in GameStop GME 0.00%↑ stock in early 2021 created a narrative of rich versus poor, big versus small, and in some eyes good versus evil.

With GME roaring again, it’s worth understanding why short selling exists at all, whether the current narrative is accurate — and indeed whether it’s an appropriate strategy for individual investors to use. Unsurprisingly, a more sober look at short selling suggests its current perception is far too negative.

Source: Koyfin, GME rides again

The Mechanics of Short Selling

As most investors know, short selling is a bet that a stock price will go down. A trader borrows shares of the stock and then sells those shares. If the stock goes down, she can buy back the shares — ‘covering’ the short — for less cash than she received in the short sale, creating a profit. If the stock goes up, she buys it back at a higher price, and thus a loss.

Behind that simple trade is an entire industry that exists to match lenders (including index funds and brokerages) with borrowers. In most cases, the process seems relatively simple — but in actuality it’s quite complex. In February, Bloomberg columnist Matt Levine detailed the difficulty of simply settling an trade between institutions, and similar challenges can arise for short sales. The result is what is known as a “failure to deliver”, in which the short seller does not actually locate the stock she has agreed to sell.

But in most cases, particularly in stocks with low short interest (and thus healthy inventory from potential lenders like brokerages), the process works smoothly. The short seller pays a fee to borrow the shares — but notably also receives most of the interest created by the cash collateral that secures the share. And so in an environment with normalized interest rates, short sellers actually receive positive net interest on short sales with a low cost of borrowing.

Of course, the practice is also exceptionally risky. The 2021 gains in GME essentially blew up hedge fund Melvin Capital. In theory, short sales have the potential for unlimited losses, and many investors will argue that returns conversely are capped at 100%1. More broadly, short sellers need stocks to decline, and over time the average stock goes up. Selling short is a risky trade that, in general, seems to fight against the tide.

Why Short Selling Exists

Back in October, we highlighted the role of activist short sellers in the equity market. As we wrote then, the high-minded purpose of the stock market is to provide signals — to companies, to individuals, to entrepreneurs — that help the economy accurately allocate capital for the benefit of society as a whole. But without short sellers, there is no incentive for negative information to make its way into the market.

In theory, that means bigger bubbles and less accurate equity prices. In this telling, short sellers provide an important service, creating something of a brake on “irrational exuberance” in the market.

Of course, as noted above, many investors disagree with that characterization. But setting aside flowery justifications, there is a key reason why short selling does exist, and should exist: hedging.

Indeed, the ‘hedge’ in ‘hedge fund’ comes from the ability of those funds (unlike mutual funds) to sell stock short. That lowers the correlation of hedge fund returns to the market, which in turn mitigates short-term risks for hedge fund investors. For some of those investors, like pension funds or college endowments, short-term risks are material: the need to distribute capital in any environment means an inability to simply ‘wait out’ a broad market downturn.

There are more narrow applications of hedging as well. Merger arbitrageurs often short as part of their strategy to bet on (or against) deals closing. Their existence allows ordinary investors to sell on a deal announcement, with merger arbs taking on the risk (and taking a small fee, in the form of positive returns, in the process).

Convertible bond issuance would be nearly impossible without hedging. Buyers of those bonds, which are convertible into a pre-set number of shares2, can short sell to hedge their exposure to movements in the stock price. This allows more speculative companies to issue convertible debt that contains exceptionally low cash interest. During 2020 and 2021, zero-coupon convertibles (ie, no cash interest) became common. This allowed those companies to fund their growth in a much more attractive manner3.

Indeed, one repeat issuer of convertibles (albeit not zero-coupon convertibles) has been Tesla TSLA 0.00%↑. More than a few investors have pointed out the irony that Tesla chief executive officer, Elon Musk, has repeatedly criticized short selling while his company funded itself using an instrument where short selling is essentially required.

The Rise Of The “Short Squeeze”

What’s different about the current perception of short selling is that it’s come at a time when markets are rallying, not fading. The practice occasionally has been banned in the U.S. and in other global markets, but nearly always when stocks are falling. For instance, the short selling of financial stocks was restricted in September 2008.

In those scenarios, restrictions on short selling seem more logical (even if the wisdom of those restrictions remains up for debate). Short sellers can cause a short-term decline in the share price of the targets, particularly if a number of trades are put on at the same time. More structurally, they do increase the number of shares that are actually in the market, since there are two investors with a long position for each share sold short. The original buyer has long exposure to the stock, and so does the investor who bought those borrowed shares from the short seller4.

In a plunging market, when regulators are under pressure to do anything, and investors are looking for scapegoats, banning short selling seems a quick way to relieve downward momentum in the market and satisfy frustrated investors.

But as we write this, the S&P 500 has gained 83% in the last five years, and sits less than 1% off its all-time high. And yet criticism of short sellers as dishonest, manipulative, and even villainous persists. This historically would be an environment where bears were pitied rather than scorned.

Clearly, a differentiating factor this time is the rise of Internet commentary and social media. The latter trend has been blamed for many ills, of course, including political polarization. Arguably a similar dynamic has played out in investing-focused media.

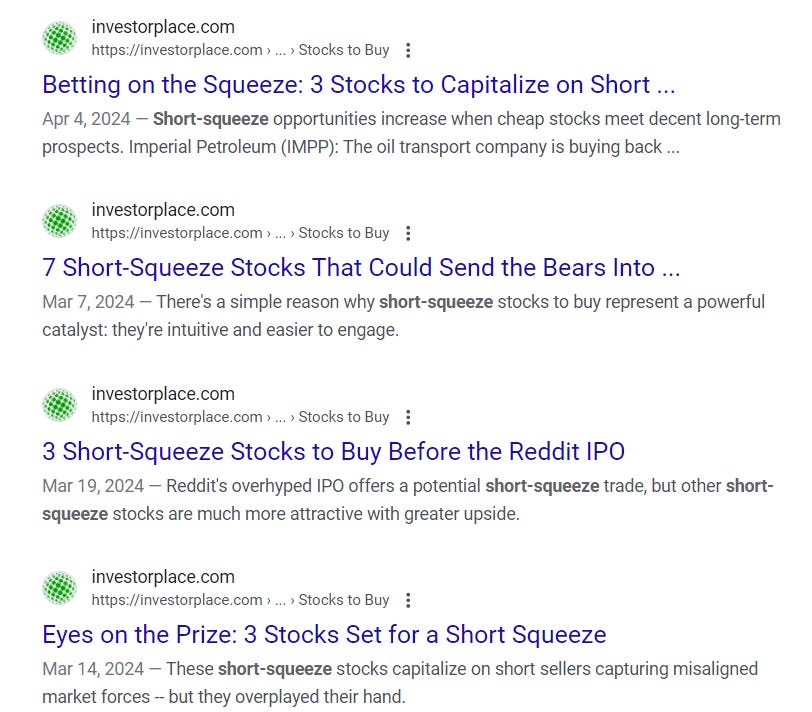

Certainly, the discussion of “short squeezes” has risen exponentially over the past decade or so. A Google search for the term on Seeking Alpha or InvestorPlace in 2014 shows exceptionally few articles focused on the topic. Over the past year, however, both sites have published dozens of such pieces:

source: Google

Yet there’s no evidence that “short squeezes” occur more often — or even really exist at all, at least in the sense that they’re commonly understood.

If a heavily-shorted stock rises after a solid earnings report, that’s not necessarily a “squeeze”. Instead, it’s simply the flip side of the valuation compression driven by the pressure caused by initial short trades.

In other words, if short selling causes price declines as the trades are entered, by definition it must cause price increases as the trades are exited. Short sellers will buy back shares to mitigate risk, which adds to the fuel from investors buying the stock on fundamentals (and also decreases the amount of shares available). That is categorically not the same thing as a short squeeze, in which short covering cascades in a vicious cycle: ABC goes to $20, so shorts buy back, which sends the stock to $22, which means more shorts have to cover, and so on.

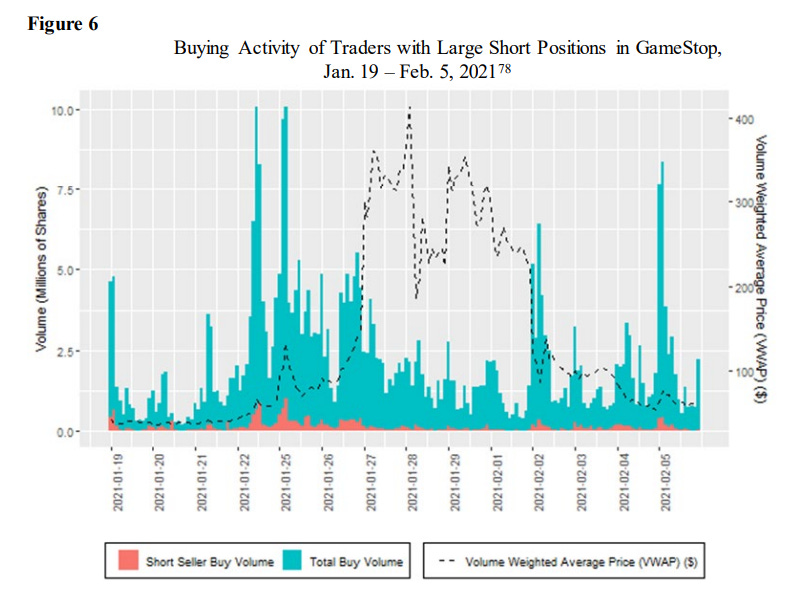

The first dynamic, in which short covering helps the stock price if the results of the business outperform, absolutely can and should be part of a bull thesis on a heavily-shorted stock. The second, however, is a trading strategy, to the extent it exists at all. Just because a stock goes up doesn’t mean there was a squeeze: even the U.S. Securities and Exchange Commission, examining industry data, could not definitely conclude that the January 2021 rally in GME was a short squeeze or a gamma squeeze5. If there was a short squeeze, it was pretty much over by the time the stock became national news; the shorts at that point were relatively new to the trade:

source: U.S. Securities and Exchange Commission

Conspiracy Theories And High Short Interest

So what has driven the sharp increase in discussion of short squeezes? We’d argue the answer is simple: it’s a compelling topic for publishers. Short squeezes create the tantalizing possibility of huge, immediate gains. And, particularly in the social media environment, they create a “heroes versus villains” dynamic that is much more fun, to put it simply, than dry discussions of fundamentals. As is so often the case with social media, that dynamic seems to have gotten out of hand.

It’s impossible to discuss this topic without at least addressing the narrative around short selling in some corners of the market. Some forms allege massive manipulation by multiple market participants, with activities ranging from “naked shorting” to the dissemination of false information to the creation of ‘fake’ or ‘synthetic’ shares of stock.

It would take another entire series of articles to dispute many of those claims. We discussed many in a piece a little over a year ago, as Bed Bath & Beyond headed into bankruptcy. So committed were BBBY shareholders that they bought shares from the company despite its obviously dire prospects; those hundreds of millions of dollars in capital simply went to modestly improve the recovery of creditors.

But the broad argument is simple: anyone who has spent any time around the financial industry would instantly know that there’s no possibility of collusion. If any hedge fund was creating a massive undervaluation in a security, or just leaving itself vulnerable to a painful squeeze, any fund that could would take the other side of the trade in an instant6.

For the most part, all of this discussion is a distraction. High short interest does have value as an indicator — but only as part of a bull case. It’s worth noting in the sense of risk: educated traders clearly are betting against the stock, and at the least an investor needs to (emphasis on “needs to”) understand why that it is. And, again, high short interest can increase near- to mid-term returns thanks to covering, as seen in the likes of GME and Carvana.

Focusing on short interest to the exclusion of other factors, however, is generally a recipe for disaster. Investors can certainly get lucky in meme stocks and high short interest plays, as has been the case this week. But no one could have foreseen the catalyst: the return of Keith Gill, a.k.a RoaringKitty, which has sparked a massive rally in meme stocks.

The enormous irony which so many meme traders miss is that Gill’s original case had little to do with a short squeeze, and certainly did not center on a MOASS (Mother Of All Short Squeezes). Instead, as Gill detailed in testimony to Congress, he believed that GameStop was an attractive turnaround play.

RoaringKitty didn’t believe the shorts were evil; he believed they were wrong. He was making a fundamental case — and that is really the only way to make reliable judgements over the long term.

As of this writing, Vince Martin has no positions in any securities mentioned, though he does kind of wish he was long GME.

Disclaimer: The information in this newsletter is not and should not be construed as investment advice. Overlooked Alpha is for information, entertainment purposes only. Contributors are not registered financial advisors and do not purport to tell or recommend which securities customers should buy or sell for themselves. We strive to provide accurate analysis but mistakes and errors do occur. No warranty is made to the accuracy, completeness or correctness of the information provided. The information in the publication may become outdated and there is no obligation to update any such information. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Contributors may hold or acquire securities covered in this publication, and may purchase or sell such securities at any time, including security positions that are inconsistent or contrary to positions mentioned in this publication, all without prior notice to any of the subscribers to this publication. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.

There is an argument that returns can be greater than 100%. Imagine a trader shorts $10,000, or 1,000 shares, of ABC at $10 per share. ABC then drops to $8; our trader can short additional 250 shares at $8, and still have the original $10,000 at risk. Should the stock go to $0, she has made $12,000 ($10 per share on 1,000 shares and $8 per share on the additional 250), or 120%. But this may be a largely semantic argument over whether the incremental short at $8 is an additional trade made after the first trade profits.

This is true for essentially every established borrower. More speculative issuers may allow for exchange into a certain dollar amount of shares, but this is dangerous: those types of bonds are known as “death spiral convertibles”. As the share price drops, the company is obligated to issue more shares, which means existing investors will be diluted, which can lead the share price to drop even further, and so on. Trump Media & Technology Group DJT 0.00%↑ used a form of this convertible — albeit one with a floor that capped the amount of shares that would be issued.

The way to think about this is that the interest is ‘paid’ in stock — or rather, the upside in the stock — rather than in cash. Convertible issuers can then mitigate the risk of giving away upside by buying call options in a so-called “capped call” transactions. The net result of that complicated transaction is lower overall borrowing costs.

This can repeat, one reason why short interest in a stock can actually exceed 100%: our second buyer too can lend her shares to a third buyer, and on and on.

A gamma squeeze is driven by hedging activities of market makers in option markets; they sell call options and buy stock to manage their upside exposure. In theory, if there is a flood of buying of call options, those market makers will be forced to keep buying the underlying stock. Emphasis there on “in theory”.

Indeed, many hedge funds were quick and smart enough to get on the long side of GME in the fourth quarter of 2020 and January 2021, adding to the pressure on those short the stock.