Carvana Stock Still Looks Like A Short

Even after a 78% decline, there's room for bearish bets on CVNA to play out

The conventional wisdom is that short sellers generally try to short stocks when they’re already on the way down. Like many pieces of conventional wisdom, that claim no doubt is not 100% accurate, but there’s some basic underlying truth to it.

The idea is that the risk of trying to precisely top-tick an overvalued stock — and getting run over if getting the timing wrong — simply isn’t worth the added potential gains from maximizing the downside in the stock. It’s better to see the stock roll over, to see the story in the market change, and trade a few points of gain in return for (theoretically) an easier path to profits, and less stress in “fighting the tape.”

Clearly, many potential short targets have long since passed that point. In our bull case on 1-800-Flowers.com (FLWS) last week, we noted that the median small-cap was 28% off its 52-week high. Just a week later, the figure (as before, according to a screen on finviz.com) is just shy of 30%.

In the universe of small- and mid-cap stocks, nearly a quarter have been at least halved from 52-week highs; go back to February 2021 (when many sectors actually topped out) and the proportion no doubt is higher. In the groups/sectors most likely to be bubbles — de-SPACs, electric vehicle stocks, speculative growth (and, in some cases, all three) — the carnage has been far more spectacular. The median 2020-2021 de-SPAC for instance, now trades below $5, more than 50% below the $10 merger price.

But those declines don’t on their own mean that investors can’t look in those areas for short opportunities. After all, the (theoretical) upside to any short sale remains a 100% gain. And while the conventional wisdom suggests it’s best to short after the story changes, there’s nothing intrinsically wrong with shorting even well after the story starts to look broken — particularly when the equity still has a sky-high valuation.

The Case For Getting Short (Anything) Here

Market sentiment seems like it rolled over the past week. In our first post on this platform, we noted that the market essentially just didn’t ‘feel’ right. We were far from alone in expressing that view, to the point that at the time the most logical reason for being bullish seemed to be only that everyone else was so bearish, too.

At least in the short-term, however, the ‘easy’ bear case has been correct. In the three weeks since that post, the Russell 2000 has dropped 6%, and the S&P 500 a touch less, and outside of sectors like energy and staples the sell-off has been far worse.

The risk a few weeks ago was that we were repeating the middle of 2007. That year, anyone paying attention knew something was up, but many felt there were still bargains to be had and/or that the market could dodge knock-on effects from housing prices, consumer behavior, etc. We’ve been no exception to that (over)confidence: we’ve made three bullish calls on this site so far, and, to be blunt, they’re all underwater.

It was in early August of 2007 that CNBC’s Jim Cramer made his famous “they know nothing!” rant on live television. Say what you will about Cramer (and he’s lost some off his fastball in recent years) but he was right:

We are going to have thousands of people, we have thousands of people losing their homes right now. Fourteen million people took a mortgage in the last 3 years. Seven million of them took teaser rates or took piggyback rates. They will lose their homes. This is crazy.

Financials got crushed almost immediately from that point:

source: YCharts

On Aug. 3, 2007, the day of Cramer’s rant, shares of Countrywide Financial — one of the biggest beneficiaries of, and participants in, the housing bubble — closed at $25.00 even. Shorting Countrywide based on the same thesis expressed by the voluble CNBC personality would have been an excellent trade; Countrywide shares would close at $4.25 on Jun. 30 of the following year, providing an 83% return.

But here’s the thing: Countrywide stock would have been a good short pretty much all the way down. Had an investor waited two months, to see more evidence of excess in the mortgage market, she would have made 70%. Had she waited until the first session of the New Year, she’d have profited more than 50%.

Had she sold CFC stock short on Jan. 9 — the day before the company agreed to be acquired by Bank of America (BAC) in an all-stock deal — she still would have generated a 17% return in less than six months, before the BAC/Countrywide deal closed on Jun. 30. The S&P 500 declined 9% over the same period.

That brings us to Carvana.

Too Far Down

It is perhaps tempting to assume that with CVNA stock now down 78% (!) from its 52-week high, and 64% year-to-date, that the short trade is no longer intact, or that there are better options elsewhere.

That’s true even for investors aware of the danger of anchoring bias, the sense that stocks are ‘cheaper’ when they’ve declined and ‘expensive’ when they’ve risen (as investors with that sense simply are ‘anchoring’ to a previous price). Fundamentally, the risk/reward simply is different at $84 than it was at $377.

But Countrywide is an example of what can happen to the biggest beneficiaries of a bubble. And Carvana certainly seems to have been one of the biggest beneficiaries of what certainly seems like a bubble in speculative and/or growth stocks that ran (roughly) from September 2020 to (in CVNA’s case) the third quarter of 2021.

What distinguishes Carvana, however, is how much the growth in its business was intertwined with the same factors boosting its stocks. It was the conditions of the post-pandemic period — among them, what Matt Levine dubbed the “boredom market hypothesis” — that drove at least part of the growth-at-any-price mentality. And it was the conditions of the post-pandemic period — most notably, low interest rates and the plunge in new vehicle manufacturing — that drove Carvana’s results higher.

Just as Countrywide stock benefited from a bubble in its end market, and a bubble in the stock market, so did Carvana. And it seems likely that from here, CVNA stock may well follow the same trajectory as CFC stock — only without a desperate white knight to save it.

Carvana Vs. CarMax

In considering CVNA’s valuation, it’s worth comparing Carvana to CarMax (KMX), the nation’s largest used-car retailer. Carvana closed Q1 with net debt of ~$6 billion; its market cap should be just shy of $15 billion. (It’s difficult to pin that latter figure precisely until the 10-Q is filed.) But along with Q1 results, the company announced the issuance of $2.25 billion in equity (an upsized $1.25 billion common stock offering along with $1 billion preferred), plus $2.275 billion in incremental debt. Most of those proceeds will go to fund the previously-announced acquisition of the ADESA auction business.

Pro forma for the post-quarter activities, Carvana has a market cap of $16 billion, and net debt (including the preferred) of $7.4 billion, for an enterprise value of $23.4 billion. CarMax, at the end of its fiscal Q4 (ending February), had a market cap of $14.8 billion and an enterprise value of $18 billion.

The fact that Carvana still is valued higher than CarMax — which had 4% of the notoriously fragmented used-car market (cars age 0 to 10 years) in calendar 2021 — is interesting. Bulls likely would argue that Carvana should be valued higher, for the same reason that Tesla (TSLA) is worth more than General Motors (GM). The company with a growth rate that suggests it will be the leader should be worth more than the company set to be passed.

Carvana indeed is outgrowing CarMax, posting revenue growth of 129% in 2021, against 68% for its larger rival in its fiscal year that ended two months later. But the gap is still large: after Carvana’s Q1, CarMax’s trailing-twelve-month revenue is still more than double that of Carvana.

But let’s give Carvana the benefit of the doubt, and assume that it indeed passes CarMax in, say, 2026, five years out. CarMax itself is targeting revenue of $33 billion to $45 billion in its fiscal 2026 (which ends February of that year); so we’ll credit it on the high end with $47 billion in FY27 revenue.

In a February presentation titled “Introduction to Carvana,” that company detailed long-term targets for Adjusted EBITDA margins of 8-13.5%. If Carvana indeed passes CarMax, and that latter company is at $47 billion in revenue in FY26, we can credit Carvana with, say, $50 billion in CY26. 13.5% margins suggest Adjusted EBITDA of $6.75 billion. KMX at the moment trades at a mid-9x multiple to its EBITDA (adjusted in the same way that Carvana would, including adding back share-based comp).

So if Carvana a) passes CarMax in revenue and b) hits the high end of its EBITDA margin targets, the stock is a big winner, and we can see at least a bit (emphasis on ‘a bit’) of what drove the stock to such highs last year. The argument then was that CVNA could grow into a $300-plus stock by being the best, and most profitable (CarMax does EBITDA margins of ~7%), used-car retailer in the country. And assuming that $6.75 billion in FY26 EBITDA, and a mid-teen multiple (presumably Carvana’s growth doesn’t plateau at precisely that point), the stock discounted back at 10% is worth ~$350.

The Fundamentals Still Look Weak

But here’s the catch. Quite obviously, that scenario is best-case, and maybe beyond best-case. Investors now do not have — and should not have — any confidence in those metrics being hit any time soon, if at all. The used car market is going to stall out amid higher interest rates and resurgent competition from new-car sales. CarMax — again, the largest player in the space — is targeting four-year revenue growth (total, not annualized) of 3% to 41%.

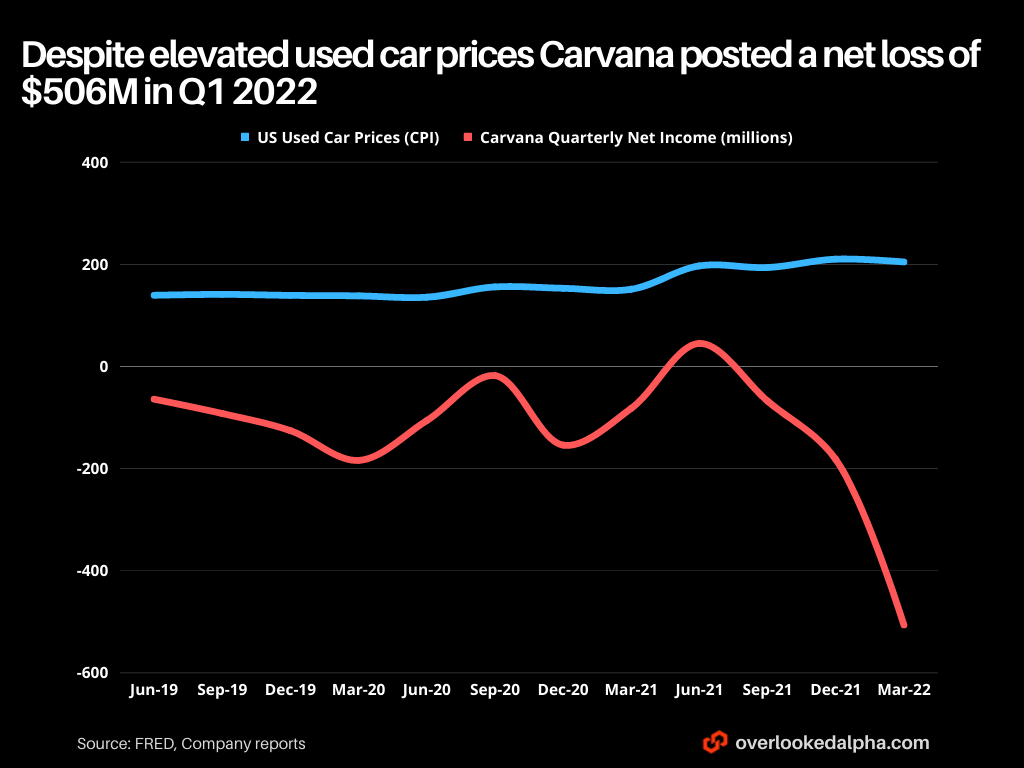

CarMax’s own outlook seems to suggest stagnant industry growth — at best. In that context, it would be impressive for Carvana to double revenue by 2026, let alone drive the 150%-plus (at least) growth needed to catch the leader. The acquisition of ADESA will help, presumably, but it’s not as if the company has a ton of whitespace left. In the recent presentation, Carvana said it covered 81% of the U.S. population, and it expects that figure to rise to 94% post-ADESA, per the Q1 call. Without greenfield growth, the nearly-exponential top-line growth Carvana has posted in recent years is going to slow. Indeed, it’s doing so already: the company just posted year-over-year growth of only 14% in Q1.

As for EBITDA margins, Carvana hasn’t even proven it can be profitable. Margins were zero in full-year 2021; they then compressed a full 9.5 points year-over-year in Q1 (excluding the impact of shares gifted to employees). On the call, Carvana chalked up the compression to impacts from higher interest rate spreads on loan sales, with the issue not necessarily being that rates moved higher but how quickly they moved higher . A cited $600-plus per unit hit accounts for all of the EBITDA loss, and then some.

That said, Carvana also benefited from prices that seem increasingly unlikely to hold. And in retail gross profit per unit, potential headwinds arose. Retail gross profit took a big hit (again, per the call) from rising reconditioning and inbound transport expenses.

Those expenses probably aren’t going anywhere any time soon, given what appear to be structural changes in labor and fuel costs. More importantly, they undercut the supposed edge of the Carvana business model against CarMax or traditional dealers. Carvana is supposed to be capital-light, lower-cost, and better-service because it doesn’t have the overhead of those old-fashioned rivals.

If that edge is gone, then Carvana’s margin profile converges toward that of CarMax or AutoNation (AN), whose margins were 8% last year during one of the best years in the industry’s history. (That stock is trading at less than 6x forward earnings, which highlights the margin compression being priced in.) From a valuation perspective, mid-single-digit margins aren’t getting the job done here.

There are a lot of moving parts here; reasonable investors can have varying opinions on both the overall market, Carvana’s share, and what margins look like. But even with CVNA stock off 78%, after Q1 it’s pretty difficult to argue that the stock is obviously ‘cheap’ from a fundamental perspective. This is a stock still pricing in pretty substantial market share gains plus relatively rapid margin expansion over the next few years — yet with far less compelling evidence for that kind of outlook.

What Goes Wrong From The Short Side

Like any trade, there are risks worth keeping in mind here, beyond the standard "shorting is dangerous, and your losses are theoretically infinite.”

For one, the price action in CVNA last week was somewhat odd. Earnings clearly disappointed. Carvana went from guiding for breakeven Adjusted EBITDA from Q2 to Q4 to that target being “pushed back a few quarters.” The equity raises needed to fund ADESA were a noted change: at the time the acquisition was announced, Carvana said it had “received committed financing of up to $3.275B from JPMorgan Chase Bank N.A. and Citi.” Less than two months later, those banks to at least some degree backed away.

Carvana delivered bad news in a plunging market. Yet the stock fell ‘only’ 10% over the following two sessions. That seems a bit of a surprise, and suggests that at least some buyers (almost $3 billion worth of buyers, actually) see Q1 as largely/mostly a short-term issue. It’s also possible that the capital raises had a beneficial effect; Carvana is getting $1.9 billion in net cash post-ADESA, and will have nearly $1 billion in real estate it can finance as well.

Second, market sentiment may well shift. If the contrarian bet three weeks ago was to be bullish, it’s now to be bullish in force. CVNA is the kind of stock with the potential to snap back quickly if rate worries moderate, or if investors return to the ‘TINA’ (There Is No Alternative) mentality to U.S. stocks.

Third, the capital raise does, indeed, strengthen the balance sheet. Carvana burned over $3 billion in 2021; it needed a capital cushion or risked having to alter its business accordingly. As even management admitted after Q1, the company got a little too focused on growth at any cost, but it can stay aggressive from here in trying to take share. In a less bearish market, share gains might be enough to at least find a bottom.

Fourth, on the ‘feel’ front, there is a sense in which the case is a little bit too easy. At least anecdotally, CVNA bears seem much like TSLA bears (and there’s definitely a good deal of overlap between the two groups). The short theses for TSLA in 2018 and CVNA in 2022 both saw the target as an unprofitable company that:

wasn’t as good as it claimed to be;

was facing well-capitalized competitors who would pivot (legacy automakers to EVs, legacy dealership groups to online);

traded at a ridiculous valuation based on near-term metrics;

and was likely to never actually turn a profit.

TSLA turned out to be a widowmaker short. I’m skeptical CVNA could ever do quite the same, but there is a scenario here where better-than-feared Q2 results put the market’s focus back on the long-term opportunity, and from there improved execution gets the stock back on track.

Worth The Risk

All that said, the short case for CVNA still seems attractive here. Yes, the balance sheet is improved, but it’s still weak. $4.9 billion in liquidity ameliorates cash burn concerns. It doesn’t end them, as the bond market shows:

source: FINRA.com

After the capital raises were announced, one debtholder told the Wall Street Journal, “If you’re an unsecured bondholder, you’re breathing a sigh of relief.” But bond prices actually didn’t move that much, and even in a higher-rate environment 9%-plus yields are pricing in some default risk.

Price action last week might suggest some strength — but CVNA fell into earnings as well. Shares still fell 17.5% for the week.

Q2 earnings may improve. But if they don’t, CVNA is going down big. And there’s a case for the ADESA side of the story to start failing almost instantly. Here’s what Lithia Motors (LAD) had to say about ADESA on their most recent call:

Yeah. We're kind of benign to [the acquisition by Carvana]. I mean we haven't given specific instructions like I believe there is now seven manufacturers that have pulled cars from ADESA, important to remember, and I believe the rest are planning to do it soon, which is part of that profit stream. I would also remember that ADESA lost money pre-COVID and [Technical Difficulty] money during COVID.

Poor initial performance by ADESA not only hurts the fundamentals/growth case for CVNA, but also adds to no-doubt-growing questions about management.

Market sentiment may change. But in that scenario, other stocks are going to rally as well; if not, CVNA seems likely to underperform even a falling market.

At the end of the day, the short thesis here is simple. Carvana is an unprofitable company with an unproven business model, and management which admitted after Q1 that it had made errors along the way. Yet it’s still valued, including debt, at well more than $20 billion.

The fact that the valuation was once over $70 billion doesn’t change that thesis; it doesn’t affect it all. There’s likely still more downside ahead.

As of this writing, the author has no positions in any securities mentioned. We may initiate a short position in CVNA in the future.

Disclaimer: The information in this newsletter is not and should not be construed as investment advice. Overlooked Alpha is for information, entertainment purposes only. Contributors are not registered financial advisors and do not purport to tell or recommend which securities customers should buy or sell for themselves. We strive to provide accurate analysis but mistakes and errors do occur. No warranty is made to the accuracy, completeness or correctness of the information provided. The information in the publication may become outdated and there is no obligation to update any such information. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Contributors may hold or acquire securities covered in this publication, and may purchase or sell such securities at any time, including security positions that are inconsistent or contrary to positions mentioned in this publication, all without prior notice to any of the subscribers to this publication. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.

Vince, what's your view on $CVNA at the present (Aug 2023)? You called the short correctly last year but any updated view here given the turnaround seems to be working (at least that's what the market believes)?