The Sell-Off In NeoGames SA Has Gone Too Far

Short-term bumps shouldn't keep investors from an enormously attractive long-term case

Update 5/15/2023: NeoGames SA is being acquired by Australia's Aristocrat Leisure for $29.50/share. That’s 122.9% above our entry price. We have now removed the paywall on this write-up.

The long-term case for NeoGames SA (NGMS) seems almost too easy. NeoGames is the leading iLottery provider in North America, with 67% market share. Contracts in Austria and Czech Republic underpin a decent international business as well. The iLottery market has grown sharply for nearly two decades at this point, yet penetration — particularly in the U.S. — remains relatively small.

Yet despite dominant share in a growing market, NGMS stock looks cheap, at ~20x 2021 Adjusted EBITDA (deducting capitalized software development costs). And an 82% sell-off from last year’s highs seems driven at least in part by the market’s sudden nervousness toward growth stocks, particularly in the small- to mid-cap categories.

That said, the short-term case against NGMS seems potentially just as compelling. 2021 performance in the company’s key US market disappointed, and for reasons that might color the longer-term story. NeoGames may well have been a “pandemic winner” in 2020 and into 2021, which raises concerns about both 2022 growth and backward-looking valuation. A pending acquisition will add leverage to the balance sheet and potentially dilute precisely that seemingly simple bull case for NGMS stock.

Those risks can’t be ignored. But at this point, it does seem like the market is pricing in all of the risks, while ignoring the story that led NGMS stock to last year’s highs. There are some short-term worries, but NeoGames remains an excellent business at an attractive valuation, and at some point the market will return to that key fact.

Introducing NeoGames

NeoGames began as a unit of Aspire Global (ASPIRE.ST) focusing on iLottery opportunities in Europe. NeoGames was spun off in 2014, two years after Illinois became the first U.S. state to offer iLottery products (instant and/or draw games offered via website/app).

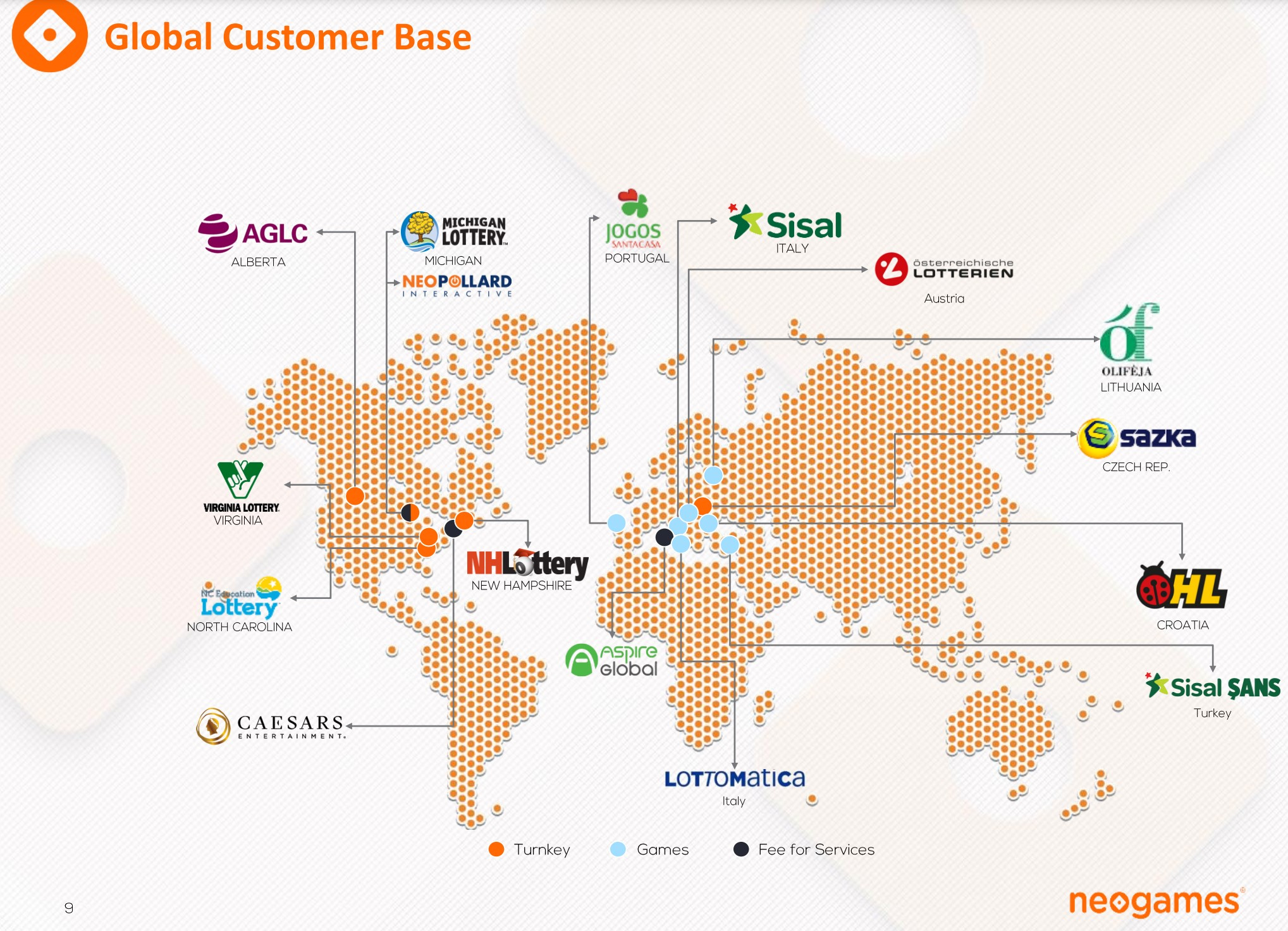

The newly independent company turned its eyes toward the American market. It scored a quick, major win in Michigan, where NeoGames became a subcontractor to Canada’s Pollard Banknote (PBKOF, PBL.TO). That contract continues: at the end of 2020, the agreement was extended to 2026. NeoGames since has expanded both in the U.S. through a joint venture with Pollard known as NeoPollard Interactive (NPI), and via independent efforts overseas:

source: NeoGames investor presentation, March 2022

The contract with Sazka, the Czech lottery, is the most important outside the U.S. But NeoGames also has agreements with a few lotteries simply to provide games for iLotteries run by competitors (NeoGames has developed over 350 proprietary games, per filings.) In the U.S., beyond Michigan and other states served by NPI, NeoGames licenses its NeoSphere platform to Caesars Entertainment (CZR) for its online gambling operations, a deal that brought in $8 million in 2021 revenue (~16% of the GAAP total). NPI’s turnkey deal with the Canadian province of Alberta includes iLottery, iGaming, and online sports betting.

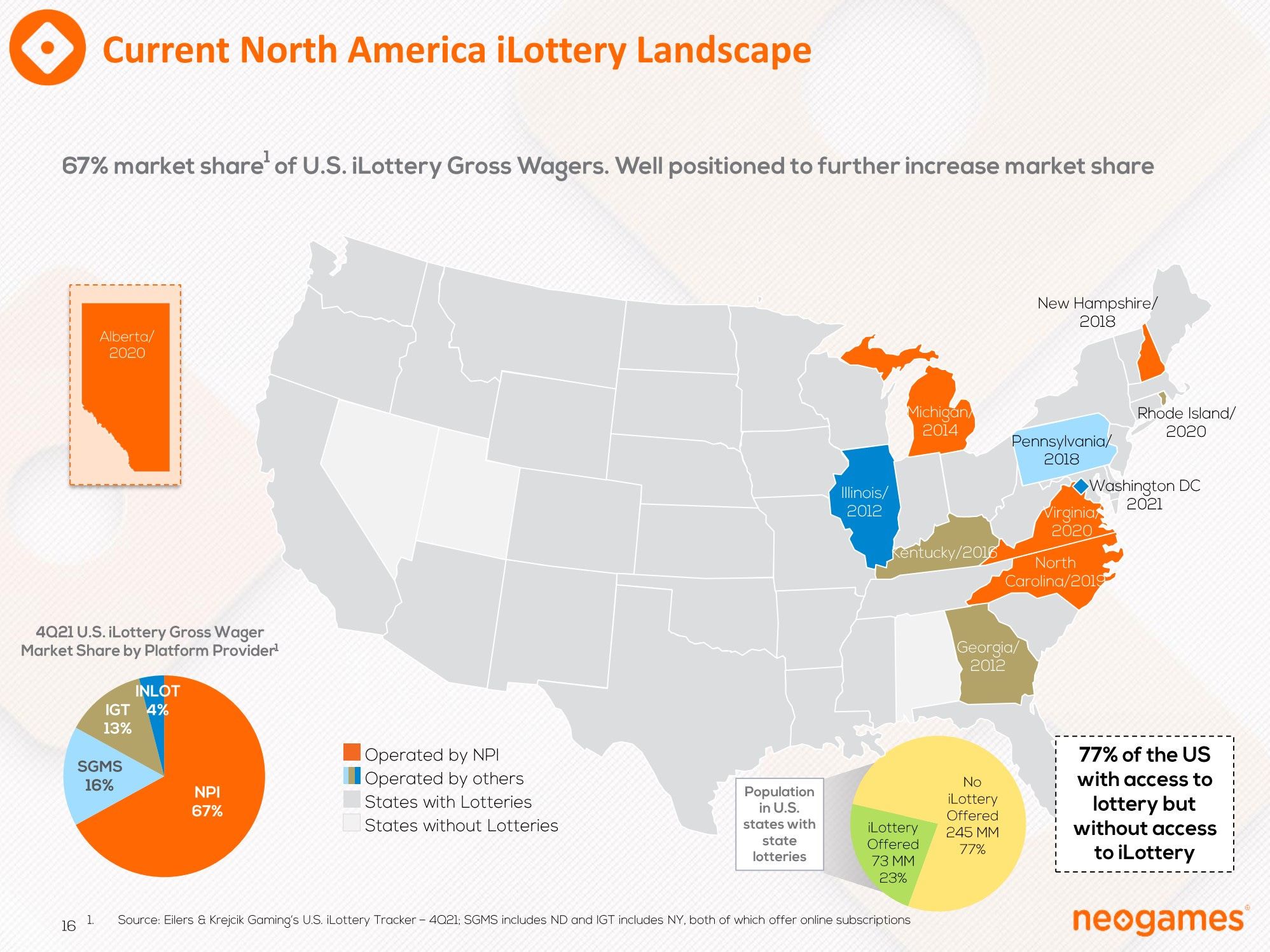

So far, NeoGames has performed exceptionally well. The company hasn’t lost any contracts (nor has NPI), while reach has steadily expanded both in the U.S. and overseas. In Michigan and Virginia, in particular, iLottery sales have soared; it appears performance there is better than in Pennsylvania, where iLottery is run by rival Scientific Games (SGMS). Overall, NeoGames has ~67% market share — and huge room for expansion over time:

source: NeoGames investor presentation, March 2022

NeoGames has done well on its own, as reported revenue nearly tripled between 2017 and 2021 (reported revenue does not include joint venture revenue; more on this in a moment). Overall EBITDA margins, excluding capitalized software development costs and accounting for that JV revenue1, are in the range of 35%; as reported, the figure neared 40% in 2021.

There’s seemingly an enormously attractive story here: success to date, strong margins, and a growing market. Indeed, that story drove NGMS above $70 less than a year ago.

Today, the stock is at $13 — not just 80%-plus off its highs, but well below its November 2020 IPO price of $17. The question is: what has caused the plunge? There are a few possible answers.

A Market Sell-Off

Obviously, an enormous change in overall market sentiment is a factor. Small- and mid-cap tech stocks have been hammered of late. A quick screen on finviz.com of Communications Services stocks (which includes NGMS) with a market cap of $10 billion or less shows that more than half are down 50%-plus from their 52-week highs. The same is true in the Technology sector.

The sell-off no doubt has come at least in part because valuations became disconnected from reality. NGMS might not be an exception to that trend. The $70 print last summer suggested a market cap around $1.8 billion — more than 20x then-expected revenues for 2021. Given margins and cash flow capabilities, that peak multiple wasn’t quite as crazy for NGMS as it was for other small-/mid-cap tech names, but in retrospect it certainly looks potentially questionable.

A 300%-plus rally in less than a year following the IPO probably was a little much. That rally could well have been amplified by a relatively thin float, which in turn could have added to the pressure on the way down (though a secondary offering from selling stockholders at $36 last year may have ameliorated the float issue a bit).

Still, it’s difficult to attribute an 80%-plus decline solely to market pressure. There clearly are other factors at play here.

Worries In Michigan

Those include company-specific concerns. Michigan is the most prominent. Revenue through NPI doesn’t run through NeoGames’ P&L; only the profits from the joint venture are added below operating profit:

source: NeoGames fourth quarter 2021 earnings release

The Michigan project, however, doesn’t run through that JV (again, NeoGames is a subcontractor to Pollard in that market). And revenue in the state declined in calendar 2021. Pollard admitted as much in its fourth quarter release. The Lottery itself estimated a 14% decline in eInstant revenue for fiscal 2021 (ending September).

Michigan is declining for a couple of reasons. Most notably, the state legalized iGaming at the beginning of 2021, providing substantial competition to online games in the state. Pollard and NeoGames also have cited post-pandemic changes in behavior; there simply are more things for Michigan residents to do besides buy online lottery tickets (essentially, to gamble) at home.

The short-term pressure in Michigan highlights two long-term worries. The first is that NeoGames was simply a short-term pandemic winner. Turnkey contracts give the company a share of revenue, and that revenue no doubt was boosted in 2020 and into 2021 by the novel coronavirus pandemic. Meanwhile, one pillar of the long-term case at the time of the IPO was that cash-strapped states would quickly expand iLottery efforts to raise revenue; that hope hasn’t panned out. So, like so many pandemic winners — including online gambling stocks — NGMS has round-tripped.

The second concern is that iLottery growth can only continue if iGaming growth doesn’t. iGaming is a better option for consumers. The take rate for states is substantially lower (meaning the expected value of the betting is far higher). The games are more varied and likely better as well. Potential expansion of iGaming in the U.S. — which has been slow, but still continuing in states like Ohio and Connecticut — thus represents a perhaps greater threat to NeoGames than investors previously understood.

There’s another possible factor, though it requires the market to be less intelligent than I generally believe it to be. (Recent history, however, suggests that perhaps I’m giving the market too much credit.) Because Michigan struggled in 2021, and because Michigan, unlike other U.S. projects, runs through the NeoGames’ P&L, the company’s reported 2021 revenue simply stalled out. Top-line growth for the year was just 2.6%, with reported revenue declining over 12% in the fourth quarter. That deceleration seems an enormous problem for a company that, again, was valued at 20x-plus revenue halfway through the year.

It’s possible that headline figure is leading investors to see a far more difficult year than 2021 actually was. Revenue from NPI, after all, soared, climbing to $34 million from $9.5 million thanks to new state launches. Add in that revenue, and NeoGames’ consolidated top line increased 43%.

Meanwhile, Michigan, per NeoGames’ per Q2 call, accounted for ~40% of turnkey project revenue that quarter, down from ~70% the year before. It’s likely that Michigan was down 20%-plus for the year2, yet NeoGames’ turnkey revenue (~60% of the total) declined only 7.3%, and, again, total revenue excluding NPI still rose for the year.

The worries about what 2021 performance in Michigan means to the future admittedly have some merit. But it also seems at least possible that to unfamiliar investors NGMS is profiling as a busted growth play in an exceptionally difficult market for small- and mid-cap growth stocks. (One small piece of evidence for this interpretation is that short interest in NGMS remains exceptionally low: the figure peaked at 1.4% low last year and now sits below 1%. That’s not the case for most similar victims of the recent sell-off.)

But growth isn’t busted. Outside of Michigan, 2021 was a solid year, given the impacts of the pandemic on year-prior comparisons and consumer behavior during the year.

Soft 2022 Guidance

Overall, these two fears seem potentially overblown. As a sell-side analyst has argued, the weakness in Michigan may be driven more by pandemic comps than by an inability to compete with iGaming. Stable revenues q/q in Q4 (per Pollard) should assuage concerns of a long decline in that state (or any other with iGaming competition). NeoGames still has plenty of opportunities for inorganic growth, including in Ohio, where management is trying to get the state to act on an already-won contract. Connecticut and West Virginia offer opportunities as well.

But there are a pair of perhaps more credible fears looking forward. For one, 2022 guidance given with the Q4 report last month seems to have disappointed the market:

source: YCharts

And the guidance does look soft. Including the contribution from NPI, NeoGames is guiding to $90 to $97 million in revenue this year. That’s an increase of just 6.5% to 14.8% against the 2021 print. Given some slippage in EBITDA margins as the year went on, the outlook suggests flattish EBITDA in 2022 versus 2021.

That follows a 2021 that, while strong overall, saw deceleration as the year went on. (In Q1, revenue including NPI increased 114%; in Q4 just 15%.) Once again, “busted growth” concerns rear their head. After all, there are some inorganic growth drivers in 2022: games delivered to the lottery providers in Turkey and Italy; incremental William Hill licensing revenue; the launch of online sports betting in Alberta. Given those tailwinds, investors no doubt were expecting more in the way of growth this year.

The Aspire Acquisition

There will be a good chunk of inorganic growth, however. Eight years after being spun out from Aspire, NeoGames is acquiring its former parent in a deal initially valued at $480 million.

The effective price is coming down steadily along with the NGMS stock price; at Friday’s NGMS close of $13.02, NeoGames is paying just $339 million3.

For the most part, the market seemed to accept the deal as reasonably wise for NeoGames. NGMS stock did slide 2.44% on Jan. 18, the day after the offer was announced, but broad markets fell that day as well (and indeed for much of that week). But in conjunction with slower-than-expected growth, the leverage funding the deal might be seen quite differently at the moment. The offer presentation suggests that the combined company will have net debt of $176 million, or about 2.5x pro forma Adjusted EBITDA.

Taking The Long View

Admittedly, there’s negativity in this case so far. And, admittedly, there’s risk. But that’s the nature of looking for long ideas in this market. This isn’t March 2009 or April 2020. The stocks down 50% were probably overvalued at their highs. The stocks down 80% have some flaws.

But from a broad standpoint, the story hasn’t really changed. The opportunity for iLottery in the U.S. and globally remains intact. NeoGames’ leadership in the space too seems unchanged. Alta Fox Capital, in a bullish note on Pollard last year, cited multiple former employees of both NeoGames and rivals who pointed to the company’s advantages in the space. Most notably, both SciGames and IGT (IGT) are building iLottery capabilities on existing, often dated stacks. NeoGames, however, is (as is often the case), the newer, more nimble, more focused competitor, even moving to cloud-based offerings where allowed by regulators. (Some states require the infrastructure to be located in-state.)

2022 performance perhaps is disappointing — but 2021 results on the top line crushed initial guidance. The volatility created by the pandemic cuts both ways. It’s far too conservative to assume that 2022 is the beginning of the end of growth, rather than simply a return to a more normal base from which growth can resume. (The same is true of the deceleration within 2021; the market was very different at the end of the year than at the beginning.) Even if iGaming competes with iLottery in states like Ohio and Connecticut, there’s still a substantial incremental inorganic growth opportunity for NeoGames from market expansion.

The Aspire deal makes strategic sense. NeoGames already is using Aspire to round out its offering in markets like Alberta; it can now offer the entire suite of options instead of just focusing on iLottery. In addition, Aspire’s Pariplay adds MGM (MGM) to the list of U.S. iGaming partners.

The lower NGMS stock price suggests a reasonable purchase price in the range of 10x EBITDA. Even assuming flat performance for NeoGames as a standalone in 2022, the combined company should trade at just over 12x EV/EBITDA4 — a multiple that already incorporates a pretty sharp deceleration in growth (and does not include any potential cost savings). Yet NeoGames is still growing revenue double-digits, and Aspire just increased revenue 31% and EBITDA 29% in its full-year 2021.

There is a catalyst problem here. As we noted in our first idea, on AppLovin (APP), this still looks like a potentially difficult market in which to time the bottom in any fallen angels (or, as we’d argue in both cases, unjustified sell-offs). Options aren’t offered on NGMS, which limits hedged plays like cash-secured puts/covered calls. NeoGames also has a large employee presence in Ukraine, another potential short-term problem.

Still, we’re not that far from where the stock found a bottom last month, and from a long-term perspective $13 remains a tantalizing entry point. Again, it’s below the IPO price. It’s 60% under the pricing of the secondary offering (~10% of shares) that closed last year. For all the broad fears, lottery spending is surprisingly resilient, and there is plenty of room for legislative activity in the U.S. and elsewhere to pick up as normalcy returns. Investors in NGMS probably have to ride out some volatility here in 2022, but looking out a few years this is a stock that has the potential to be a massive winner.

Revenue including NPI, the joint venture with Pollard, totaled $84.5 million in 2021. NeoGames’ reported Adjusted EBITDA was $33.4 million; NPI generated $25.2 million (as NeoGames’ 50% share was $12.6 million). Capitalized software expense totaled ~$16 million on the H1 run rate, as full-year cash flow statement hasn’t been filed yet. Wholly-owned EBITDA for NeoGames less capitalized software plus NPI thus comes out to ~$30 million on that $84.5 million revenue base, for margins just above 35%.

Again, the fiscal year showed a ~14% decline per the Michigan Lottery — but Q4 2020 in the state must have been strong, as NeoGames’ turnkey revenue rose 80%. Q4 2021 in Michigan was stable quarter-over-quarter, per Pollard’s release. Michigan’s plunging share in Q2 (again, 70% to 40%) came in a quarter in which overall turnkey revenue declined only 20%. Whatever the precise numbers in CY21, Michigan was down big.

NeoGames is paying 50% in cash and 50% in stock, the latter of which was originally valued at $38 instead of the current $13. Normally, that kind of share price decline would raise the risk of the deal being scuttled or at least renegotiated. But there’s a good deal of cross-ownership here: 67% of Aspire shareholders already “irrevocably elected to accept the Offer,” as the release put it. Those shareholders are taking all of their consideration in stock, leaving public Aspire shareholders an all-cash option. And so Aspire stock hasn’t budged since the deal was announced, closing Friday at SEK 107.80 against the SEK 111 offer price.

Aspire generated EUR 30.6 million, or $33 million, in EBITDA in 2021 (pro forma for its divestiture of its B2C business). NeoGames generated $17 million adding back capitalized software costs. With 7.6 million shares going to Aspire shareholders, the combined company should have 33M shares outstanding, for a pro forma market cap of $430 million. Add pro forma net debt of $176 million and EV/EBITDA is around 12.1x.

Disclaimer: The information in this newsletter is not and should not be construed as investment advice. Overlooked Alpha is for information, entertainment purposes only. Contributors are not registered financial advisors and do not purport to tell or recommend which securities customers should buy or sell for themselves. We strive to provide accurate analysis but mistakes and errors do occur. No warranty is made to the accuracy, completeness or correctness of the information provided. The information in the publication may become outdated and there is no obligation to update any such information. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Contributors may hold or acquire securities covered in this publication, and may purchase or sell such securities at any time, including security positions that are inconsistent or contrary to positions mentioned in this publication, all without prior notice to any of the subscribers to this publication. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.