Updates For Sportradar, i3 Verticals and Asure Software

We highlight three past bull calls that still look attractive going forward

💡 Highlights:

As was the case two years ago, Sportradar looks attractive, even with a seemingly full valuation. A key role in the sports betting ecosystem should drive consistent growth and solid returns in the stock.

A transformative deal for i3 Verticals delevers the balance sheet. It also opens the door to M&A — or a potential sale.

We wrote last year that our call on ASUR might be right, but early. As the company works through headwinds around a key product, that prediction seems correct.

In the midst of a market that is starting to look stretched, we return to three ideas that could have more gains ahead.

Sportradar Still Looks Like A Winner

In a different market, our recommendation of Sportradar SRAD 0.00%↑ would look like a solid pick. In just under two years since our call, SRAD has gained 30%. That’s actually modestly better than the Russell 2000 Total Return over that stretch — but 26 percentage points worse than the S&P 500 Total Return.

Looking forward, in an environment where SPY seems unlikely to gain another 56% over the next two years, SRAD seems well-positioned to provide similar returns on an absolute basis, which might well lead to outperformance this time around.

Valuation isn’t necessarily cheap on a headline basis: shares trade at a little over 16x this year’s guidance for Adjusted EBITDA1. But Sportradar has posted impressive growth, with revenue rising 20% in 2023 and guidance suggesting another 22% jump this year. The U.S. market has been a key driver — revenue more than doubled between 2021 and 2023 — but far from the only source of strength. Ex-US, Sportradar has generally grown at a 20% rate in recent years, with a high-teens rate likely in 2024.

On a qualitative basis, the valuation too looks reasonable. This is a solid business, one that has become critical to the sports betting industry globally. An excellent feature from Bloomberg earlier this month highlighted Sportradar’s role in the space. Bookmakers are increasingly leaving the business of actually setting odds to the Sportradar, as well as rivals like Genius Sports GENI 0.00%↑.

This allows the likes of DraftKings DKNG 0.00%↑ and Flutter Entertainment FLUT 0.00%↑ to focus on marketing and customer acquisition, while also limiting arbitrage opportunities. Most importantly, it allows those bookmakers to offer an ever-expanding universe of attractive and lucrative live bets:

Sportsbooks also offer a smorgasbord of odds that change in real time during games, tempting the itchy trigger thumbs that are always poised over our phones. “Bookies need to have something live at any point in time,” one industry insider told me… “To not have that would be like”—and here he paused, searching for the perfect analogy and then finding it—“Amazon not having things to sell during some points of the day.”

Investors clearly see continued growth ahead for the market as a whole, particularly in the U.S. DKNG is up 238% since the end of 2022, and FLUT (which also has a large European operation through its legacy Paddy Power arm) is +72%. With valuations for both those companies getting questionable, SRAD looks like an attractive avenue for playing that growth.

Downside And Upside

Even after the 30% gains over the last two years, the story is not all that different. There’s still a lot of growth here — and likely more growth than is priced in. Mid-teen revenue growth, some operating profit expansion, and modest multiple expansion means SRAD likely offers ~15% annualized returns going forward.

As always, there are risks. Valuation is reasonable in the context of current growth, but that growth is not guaranteed to continue. The European market is mature (and the economy on the Continent a bit uneven at the moment), while the U.S. still represents more than 20% of revenue.

Competition is another risk. GENI has been a better stock off the lows, and has driven solid growth of its own thanks to a partnership with the National Football League. The race to be the “official” data provider of various leagues can drive up the cost of data: Sportradar spent about $200 million on data in 2023, and those costs will continue to rise. At the moment, they are eating up much of the company’s operating cash flow, though executives have said they expect free cash flow will improve going forward.

There’s also the potential for competition from market makers in the financial industry. In 2022, Susquehanna took a 13% stake in Australian bookmaker PointsBet, with the goal of creating an outlet for its Nellie Analytics subsidiary, which focuses on live betting. Other firms have similar designs on the market.

Taking the broad view, however, Sportradar seems particularly well-positioned. The sheer amount of data the company has provides an edge against competition. The shift by bookmakers to third parties for odds setting will become a virtuous circle: once those capabilities are outsourced, they become incredibly difficult to bring back in-house. Bookmakers will need massive amounts of expertise to match Sportsradar’s data, algorithm, and machine learning/artificial intelligence capabilities (management has been talking up AI, and recruiting experts in the technology, since long before AI became a buzzword).

Meanwhile, the shift to live betting is likely to continue, since it’s what Sportsradar’s customers want. Founder and chief executive officer Carsten Koerl said at a conference in May that every percentage point growth in the live market versus pre-game provides well over $1 million in incremental earnings for his company. Live betting options also expand the market, further driving growth.

Qualitatively speaking, this simply seems like a good business. And while valuation is not that attractive on a bottom-line basis (net income and free cash flow will be modest both this year and likely next year as well), there’s enough room for market growth and benefits from the shift to live for SRAD to grow nicely into this valuation. This still seems like a business worth owning.

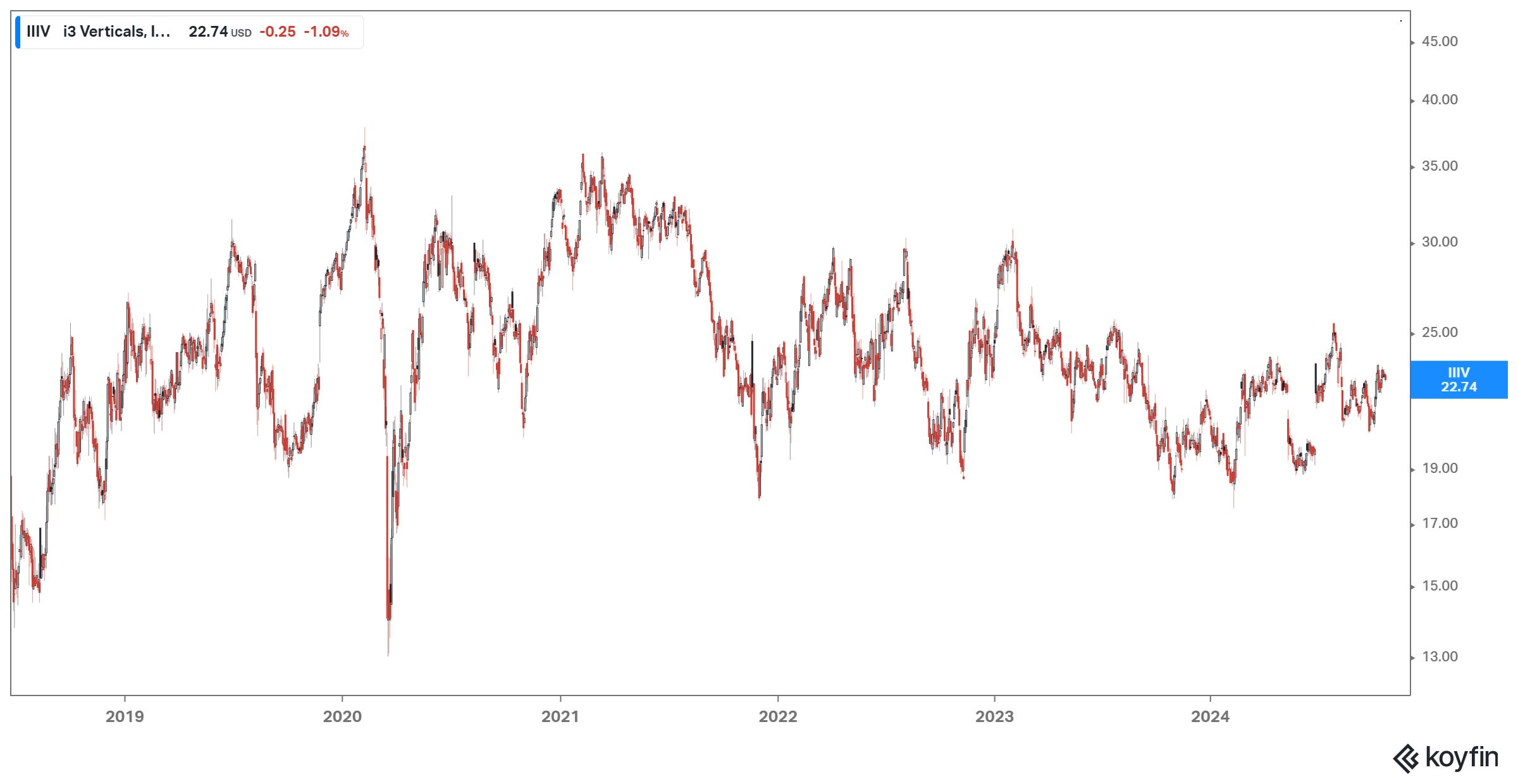

i3 Verticals Delevers — And Gets No Credit

i3 Verticals IIIV 0.00%↑, which we highlighted last November, is another stock where the story is the same — mostly. IIIV has gained 13% since our call, but overall performance for the software and payments roll-up has disappointed since its 2018 initial public offering:

source: Koyfin

Yet, as we argued last year, there’s a case that the market continues to miss the story here. Founder Greg Daily has already created two highly successful businesses in the space (both of which sold at impressive valuations), the company’s acquisition strategy seems on point, and valuation is reasonable in the context of growth.

That seems particularly true given how dramatically i3’s story has changed of late. Last month, the company closed the sale of its payment processing business to privately held Payroc for $438 million. IIIV did jump 12% when the deal was announced in June, but shares have been stagnant since.

But the sale seems to resolve two key risks that were facing the company as it headed into 2024. Most notably, it fixes the balance sheet. As of the end of Q1, the company was 3.5x net levered. The transaction, after taxes, should remove nearly all of the company’s debt.

The exit from payments also reorients i3 as a pure-play vertical software company. That’s been a niche investors are quite fond of, with winners like Veeva Software VEEV 0.00%↑. The ‘new’ i3 in fact looks a bit like EngageSmart, a stock we recommended back in 2022, which went private in a January buyout by private equity giant Vista Equity Partners.

Pro forma for the sale, i3 seems to be trading at about 12x 2025 EBITDA and a low 20s multiple to adjusted net income. Both look attractive for guided high-single-digit growth and a balance sheet with dry powder for further acquisitions. The narrow focus on public sector, education, and health care customers should provide some protection from macro weakness, and as we noted in July, contingent consideration changes suggest the M&A strategy has been reasonably successful so far. (So does the sale, which given commentary around taxes will result in a substantial profit.)

The argument last year was that i3 simply wasn’t getting enough credit from the market. That argument still seems to hold. A growing vertical software play at a low-teens EBITDA valuation seems like it should be attractive — particularly with a newly-cleared balance sheet. Admittedly, so far the bull case hasn’t played out. But with so much P-E cash floating around, we still believe that at some point Daily will engineer a third successful, profitable, exit.

Asure Software Works Through A Problem With The IRS

When we highlighted Asure Software ASUR 0.00%↑ in September 2023, the stock had been halved in a matter of months, largely due to concerns around a key service. Asure had profited greatly from a product processing the Employee Retention Tax Credit, created as part of the CARES Act, passed in 2020.

The purpose of the ERTC was for employers to keep their employees on payroll during the pandemic. Unfortunately, in practice, the ERTC proved fertile ground for fraud; Internal Revenue Service commissioner Danny Werfel said this June that at least 70 percent of claims had “red flags about their accuracy”. And so last year, the IRS stopped processing those claims (the moratorium ended last month).

Our argument at the time was that the market was overreacting. Even before the moratorium, the ERTC was set to expire in 2025. And yet Asure lost well over $200 million in market capitalization in the wake of the announcement.

A little over a year later, there’s still a case that the market is overreacting. ASUR has gained 11% since publication, but shares still look cheap — and investors still may be spooked by the ERTC issue. On a headline basis, year-to-date performance looks soft, with revenue down 6% and Adjusted EBITDA off 24%.

But the entirety of that weakness is driven by the ERTC. First-half revenue excluding the credit was up 13.5%. On the same basis, Adjusted EBITDA almost certainly has risen; the figure is down $3.4 million while ERTC revenue is off more than $10 million. There does seem to be a growing business being hidden by a one-time headwind that should come to an end next year: ERTC revenue this year is on pace to be less than $3 million.

The Bull Case For ASUR

And so in our piece last year, we noted that our thesis “might be right, but early”. ASUR is not a heavily-traded or closely-followed name. What it looks like is a long-struggling name (shares are down 88.5% since Asure’s IPO back in 1992) posting declining revenue.

What Asure actually is, however, is a business that is continuing a successful turnaround. Much like i3, the company pivoted away from its legacy business via a sale that cleaned up its balance sheet. Asure now focuses on HCM (human capital management) software, with a particular niche with small and medium-sized businesses outside major metropolitan areas.

It’s done so successfully:

source: Koyfin

The launch of a marketplace offering, which allows for the integration of over 100 modules into Asure software, has been a success. Normalized interest rates have created profit from float of customer funds. Acquisitions have helped as well, but guidance seems to suggest organic growth in the high-single-digits, while new bookings continue to shine (+50% in 2023, +131% in Q2).

Yet valuation here seems exceptionally conservative. Based on guidance, EV/EBITDA is about 9x, a more than acceptable multiple for this kind of growth. And as the calendar turns to 2025, the ERTC headwind will abate. Investor focus should return to the core HCM business.

In that context, ASUR has a clear path toward real upside. Last year, we saw the bear case (in which organic growth stalled out) at around $7, which is where the stock bottomed earlier this year. Our base case scenario: a low-double-digit multiple to ~$30 million in EBITDA (up from ~$26M this year). That suggests a market cap of ~$350 million (11x EBITDA + $20M in net cash) and a share price around $12 (about where we were last year).

That price would suggest more than 20% gains from the current price just below $10. But the blue-sky bull case remains. In that case, investors start giving Asure credit for its turnaround and its growth. A mid-teen multiple to $35-$40M in EBITDA (a reasonable target for 2026) means the stock more than doubles (16x $37 million plus $25M net cash gets the stock to $22).

The argument for ASUR is that starting with Q1, ERTC comparisons fade and the impact of organic and acquired growth becomes more clear, driving a re-rating of the stock. For an underfollowed small cap, it can be that simple.

As of this writing, Vince Martin has no positions in any securities mentioned. He may initiate a position in these securities in the near future.

If you enjoyed this analysis please help us by clicking the “♡ Like” button.

Disclaimer: The information in this newsletter is not and should not be construed as investment advice. Overlooked Alpha is for information, entertainment purposes only. Contributors are not registered financial advisors and do not purport to tell or recommend which securities customers should buy or sell for themselves. We strive to provide accurate analysis but mistakes and errors do occur. No warranty is made to the accuracy, completeness or correctness of the information provided. The information in the publication may become outdated and there is no obligation to update any such information. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Contributors may hold or acquire securities covered in this publication, and may purchase or sell such securities at any time, including security positions that are inconsistent or contrary to positions mentioned in this publication, all without prior notice to any of the subscribers to this publication. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.

Sportradar has 318.5 million shares outstanding on a fully diluted basis (accounting for potential conversion of Class B shares held by the founder), for a market cap of $3.95 billion. Net cash is $297 million (at 1:1.09 USD:EUR), for an enterprise value of $3.65 billion. Adjusted EBITDA is guided to “at least” 204 million EUR, or $222 million, putting EV/EBITDA at 16.4x or better, presuming guidance is on point.